Two ways to trade and invest

CFDs・Share trading

Australia's No.1 CFD provider1. Trade 18,000+ markets and invest in shares with $0 commission.4

Start trading

Available on web, iOS and Android.

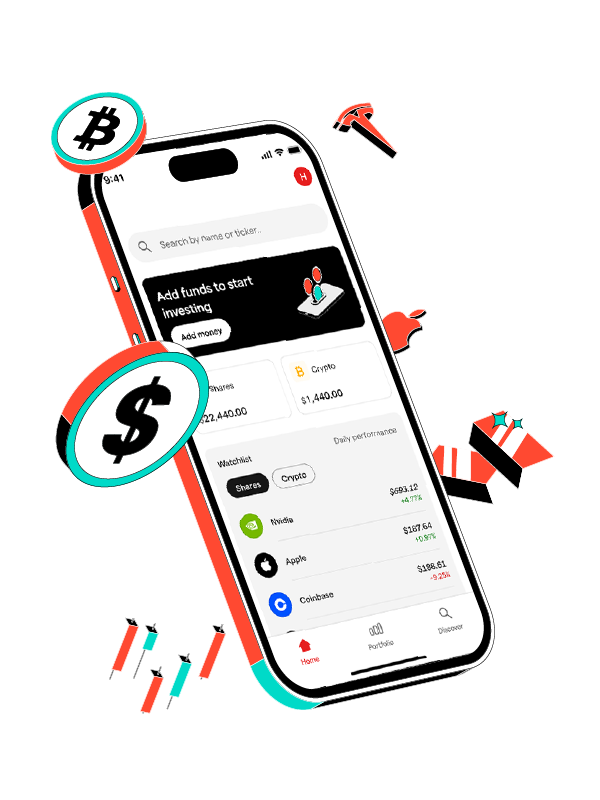

Crypto・Shares・ETFs

Invest in crypto2, shares, and ETFs, in a simple, all-in-one investing app. Get started with just $2.

Start investing

Available on iOS and Android only.

Crypto is offered by IG Digital Assets Australia and is unregulated.

IG MARKETS · NEW

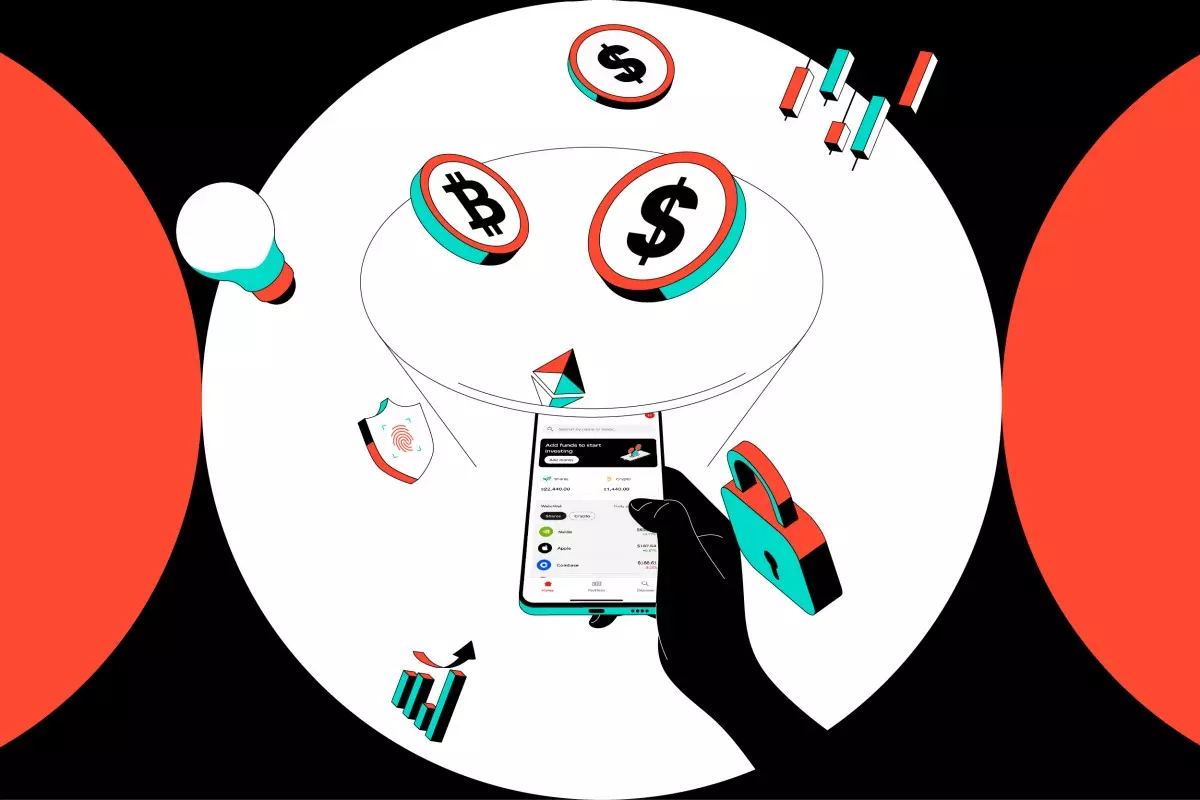

All-in-one app for shares, ETFs and crypto

Buy, hold and manage real shares, ETFs and crypto in one clean app. AUSTRAC-registered and fully reserved. Crypto is offered by IG Digital Assets Australia and is unregulated.

Built for simplicity

A clean, mobile-first app that makes owning crypto easy.

Security, sorted

Your assets stay yours. Held 1:1, independently audited and AUSTRAC-registered.

Real support

Australian specialists by live chat and WhatsApp, plus 24/7 virtual assistance.

IG MARKETS · NEW

All-in-one app for shares, ETFs and crypto

Buy, hold and manage real shares, ETFs and crypto in one clean app. AUSTRAC-registered and fully reserved. Crypto is offered by IG Digital Assets Australia and is unregulated.

Built for simplicity

A clean, mobile-first app that makes owning crypto easy.

Security, sorted

Your assets stay yours. Held 1:1, independently audited and AUSTRAC-registered.

Real support

Australian specialists by live chat and WhatsApp, plus 24/7 virtual assistance.

IG TRADING

Everything you need to trade

Trade 18,000+ markets and invest in Australian, US and UK shares with $0 commission per trade4 and only a 0.7% FX fee on international trades.

CFD Trading

Go long or short on shares, indices, forex, commodities and crypto with leverage.

Share Trading

Buy and own real Australian & global shares with $0 commission.

Platforms & tools

Web, mobile, MT4, ProRealTime and TradingView with advanced charting tools.

Learn as you go

Whether you're just starting out or sharpening your edge, we've got the tools to help you grow.

Live prices on popular markets

- Popular markets

- Indices

- Forex

- Shares

Choose an award-winning platform5

Ready to trade or invest?

Open an account in minutes and get started today.

Ready to trade or invest?

Open an account in minutes and get started today.

* T&Cs apply. Read the terms and conditions of the promo here.

1 Number 1 in Australia by primary relationships, CFDs & FX, Investment Trends November 2024 Leveraged Trading Report.

2 IG Digital Assets Australia Pty Ltd (ABN 686 210 462) is registered with AUSTRAC as a Digital Currency Exchange provider. Cryptocurrency trading is highly speculative and volatile. The cryptocurrency market is unregulated and you do not benefit from Investor protections available for regulated financial products. Cryptocurrencies are not covered by the Australian Financial Complaints Authority (AFCA) scheme. You may lose all of your investment. The purpose of this website is solely to display information regarding the products and services available on the IG Markets App. It is not intended to offer access to any of such products and services. You may obtain access to such products and services on the IG Markets App.The information on this website does not take into account your objectives, financial situation or needs. You should consider whether cryptocurrency trading is appropriate for you in light of your circumstances and seek independent financial advice before deciding to trade.

3 IG Australia is part of IG Group Holdings Plc, a member of the FTSE 100.

4All trading involves risk. $0 commission applies to clients who trade on the IG share trading account and opt for the default setting of ‘instant currency conversion’. Clients who choose to convert currencies manually will pay commission of 2 cents per share with a minimum charge of $10 on US stocks and, for European markets, we charge £10 / €10 per trade or 0.1%, whichever is higher. Other fees and charges may apply, please see our share trading cost and charges page.

5 Winner of ‘Best Multi-Platform Provider’, ‘Best Platform for the Active Trader’, ‘Best Finance App’ and ‘Best Online Stockbroker’ at the ADVFN International Finance Awards 2025; Canstar 5-Star Award for Outstanding Value – Online Share Trading for Casual Investor, Active Investor and Trader categories; Moneymagazine Best of the Best 2025: Best-Value Feature-Packed Premium Share Broker.