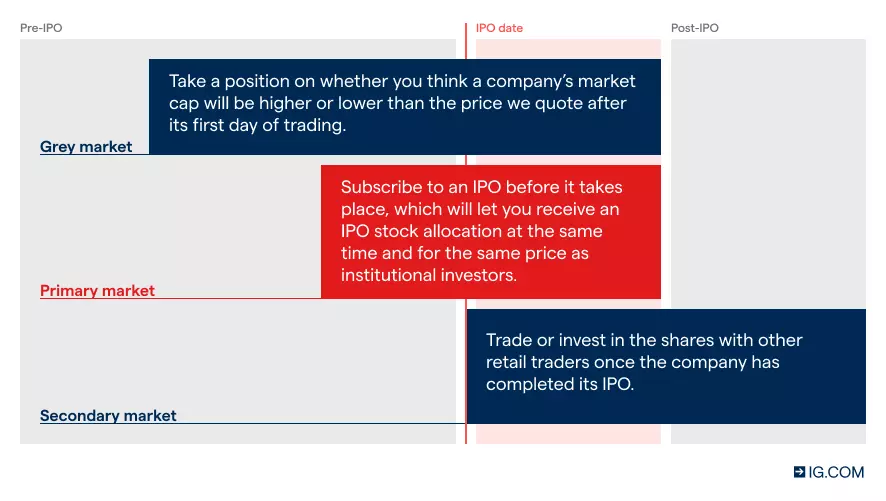

Decide how to take a position on an IPO

With us, you can invest in the company’s shares with a share dealing account on the primary or secondary market. Investing in the primary market lets you take a position on the company’s stock pre-IPO; investing in the secondary market will give you ownership of the shares once the company has completed its IPO.

You can also trade on a company’s market cap pre-IPO with our exclusive grey markets, or speculate on the company’s share price on the secondary market with derivatives like spread bets and CFDs.

Investing in shares

You can create a share dealing account to invest in upcoming IPOs on the primary market or to invest in shares once they’re available on the secondary market.

When you’re investing, you’ll pay the full value of the position up front which will give you direct ownership of the company’s stock. This’ll make you a shareholder, and you’ll be eligible to receive any dividends that the company pays, and get shareholder voting rights if the company grants them.

With us, you can invest in US shares for zero commission and UK shares from as little as £3.2

Trading derivatives

You can create a leveraged trading account to speculate on a share’s price movements with derivatives like spread bets and CFDs. Before the IPO, you can use these derivatives to trade our grey market, and after the IPO you can use them to speculate on a stock’s price rising (by going long) and falling (by going short).

You might choose derivatives because they enable you to open a position with leverage, which requires a small deposit (margin) rather than committing the full value of the shares upfront. This can magnify profits and losses, as both will be calculated from the full exposure of the trade, not just the margin you put up a deposit. Derivatives also offer various tax benefits.3