What are interest rates and how do they work?

Interest rates are a huge part of our financial landscape and affect everything we earn – and owe. Discover what interest rates are, how they work and how you can trade them with this handy guide.

Call 0800 195 3100 or email newaccounts.uk@ig.com to talk about opening an account.

What are interest rates?

Institutions who lend out money, like banks or a brokerage, typically charge a fee for doing this. The amount you pay that is on top of your loan amount, included within the loan amount, is called interest. How much interest you are charged is called the interest rate. Usually, it’s a percentage amount of your borrowed amount (for example, 10%).

What is the UK bank rate?

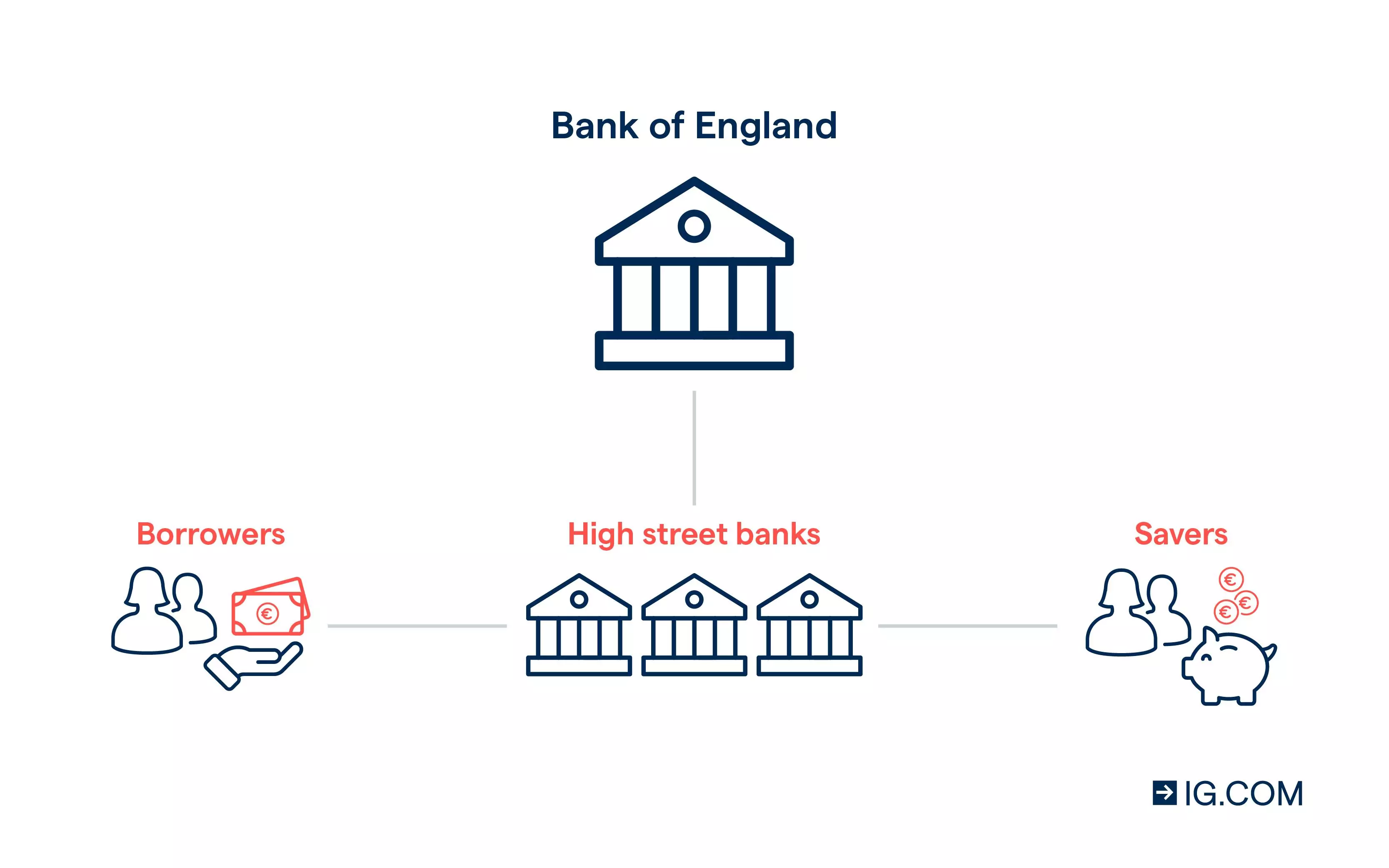

In the UK, this is the interest rate set by the Bank of England – the single most important interest rate in the UK, known as the bank rate.

All financial institutions take their cue from the Bank of England, many in turn requiring loans from the Bank of England themselves. So, whatever interest rate the Bank of England sets affects the rate at which other banks can borrow from them. This has a ripple effect onto the man in the street, as this rate will partially determine the interest rates banks and other lenders set for customers to adhere to.

How does the interest rate affect me?

The interest rate affects you in a number of ways. Firstly, and most understandably, it affects how much you’ll have to pay for borrowing. For example, if you loan £1000 and the interest rate is 7%, you’ll repay £1070. If the interest rate is a higher, say 12.5%, you’ll have to pay back £1125.

Interest rates affect your savings, too. A higher interest rate means your savings are worth more, while a lower interest rate means savings are worth less.

If you’re an investor or a trader, interest rates will affect these areas as well. Stock prices are sensitive to interest rate changes, as are other asset classes too. Property prices, for instance, are often negatively affected by increasing interest rates and positively affected by decreasing ones. Even commodity prices can take a dive during an interest rate hike.

As you can imagine, all of this has a knock-on effect for the economy as a whole. Everything from the price of consumer goods to how fast your nest egg grows will be swayed by interest rates.

What are the types of interest rates?

There are different types of interest rates, identified by who issues them. These are:

- Central bank interest rates –national interest rates adopted by a country and determined by that country’s central banking authority. In the case of the UK, that’s the Bank of England. In the United States, this is the Federal Open Market Committee (FOMC)

- Bank account interest rates –interest rates set by local or regional banks, which are affected by the central bank’s rates

- Mortgage interest rates –rates on loans, such as home loans for those buying a new house, given out by lenders like banks

How do interest rates work?

Interest rates come part and parcel with the loan you’ve taken out, or as part of the savings you’ve amassed. In the case of a loan, your total loan repayments plus the calculated interest amount would be divided into a monthly sum for you to pay (as a minimum amount – you can always pay more).

In the case of savings or investments, the interest rate would be the amount that your savings appreciate each year. Either way, the interest is indivisible from the total amount – and the interest rate is how much that amount grows by.

Example of interest earned from savings

If you have money stored in a secure facility that has a growth rate each year, such as a longer-term savings facility with your bank, the amount by which your wealth grows is its interest. Essentially, the bank is paying you in interest for keeping your savings int hat account with them.

Let’s say, for example, that the growth rate of that particular savings facility is 5%, and your savings to begin with come to £1000. Your savings then accrue 5% interest each year from the bank (which would be £50 for the first year) leaving you with £1050 by then.

Example of interest charged on borrowing

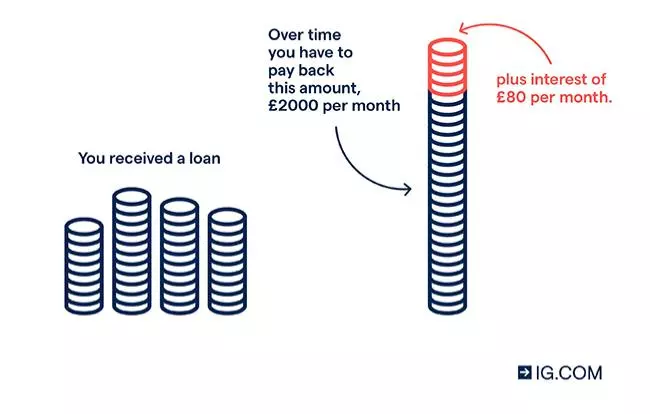

The same is true of a loan. Let’s say you approach your bank for a home loan of £100,000. If the bank grants you that loan, they will charge a certain amount of interest on top of the loan. This may be worked out as a fixed amount, a variable amount that depends on economic conditions or a percentage payable annually, among the various types of loans you may acquire.

Let’s say you get a fixed loan for £100,000 with fixed interest rate of 4%, with monthly payments calculated on the length of your loan. If you were to take out the loan for a 50 month period, you would not only have to pay £2000 each month (£100,000 divided by 50 months) but an additional 4% of that monthly amount (£80) payable due to interest. So, you would have £104,000 (£2080 x 50 months) to repay for a £100,000 loan.

What is APR and how does it differ from interest rates?

'APR' is the Annual Percentage Rate charged by lenders, which is different to your interest rate.

A lender like a bank will often also charge small additional amounts for services rendered over and above the interest. Examples of this would be a fee for opening the mortgage at the start or closing it when the loan term is up, or broker fees.

For this reason, lenders advertise an ‘APR’ rate, which gives you the total cost of both the interest and any of these additional payments in one amount. It is often a more accurate way of depicting the true cost of your loan, without any hidden fees lurking.

What is compound interest and how does it work?

Compound interest is a wealth generation phenomenon, where your interest on savings begin to earn interest. This ‘interest on top of interest’ means that your money continues to grow itself.

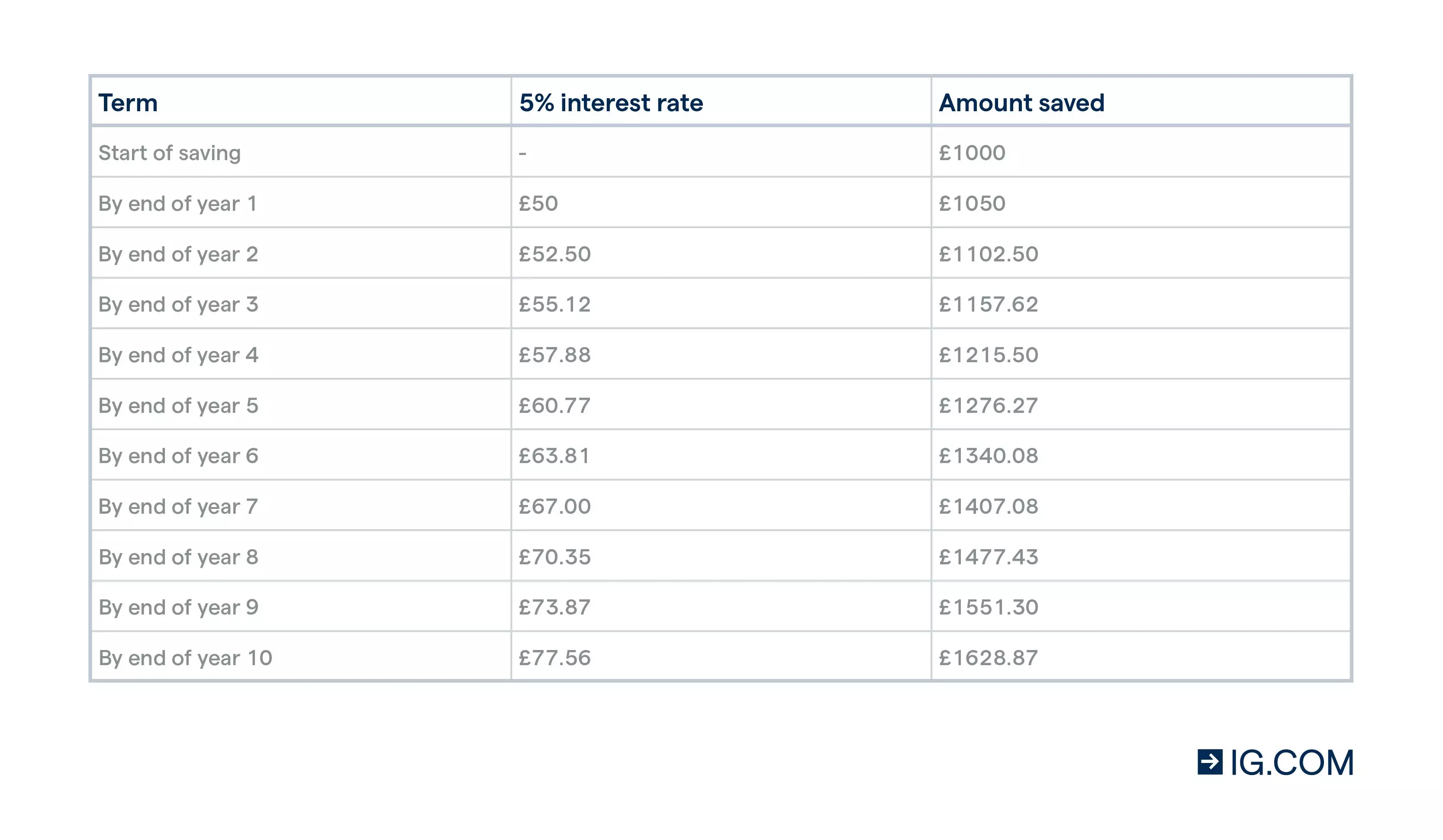

Let’s look at our previous example to illustrate this better. If you have £1000 in a savings facility where the interest means it grows by 5% per annum, that would be £50 for the first year. However, this does not mean your savings grow by a static £50 each year – instead, in your second year, your amount will now grow by 5% of £1050, which is £52.50. In the third year, you would earn 5% interest on £1102.50. By the end of the tenth year, your £1000 has grown more than one and a half times to over £1600.

As you can imagine, this has a snowball effect and gets exponentially bigger over longer periods of time.

Compound interest is a wealth generation phenomenon, where your interest on savings begin to earn interest. This ‘interest on top of interest’ means that your money continues to grow itself.

Let’s look at our previous example to illustrate this better. If you have £1000 in a savings facility where the interest means it grows by 5% per annum, that would be £50 for the first year. However, this does not mean your savings grow by a static £50 each year – instead, in your second year, your amount will now grow by 5% of £1050, which is £52.50. In the third year, you would earn 5% interest on £1102.50. By the end of the tenth year, your £1000 has grown more than one and a half times to over £1600.

As you can imagine, this has a snowball effect and gets exponentially bigger over longer periods of time.

Compound interest works the other way, too. If you were to take out a loan of £2000 with an interest rate that meant the interest compounded 20% annually, after just three years, the total payable amount would be £3456 – almost double your loan amount – as 20% of the total keeps growing in size with each year.

How are interest rates decided?

Interest rates are decided by the central banks, whose decision will have a trickle-down effect to the lenders and their clients. Central banks will set a target interest rate depending on a number of macroeconomic factors.

For example, in a period of depressed economic growth (such as during Coronavirus pandemic), central banks may keep interest rates flat or cut the interest rate, to encourage more consumer spending and saving in a financially difficult time. This is known as a ‘dovish’ stance. Interest hikes can occur in a time when the economy is picking up, which is known as a ‘hawkish’ stance.

Other factors include:

- Influential economies’ interest rates

- Inflation

- Governmental monetary policy

Interest rates for traders and investors

On a surface level, a higher interest rate will mean more profit for investors, as the rate at which their investments grow is accelerated.

For traders, however, this goes deeper, as the very conditions around changing interest rates are waves and swells in the market that can be traded for profit – or at a loss. A sudden change in interest rate stance can lead to much volatility in the marketplace, which can be an opportunity to trade.

For this reason, most traders and investors will watch interest rates and the discussions around them with great interest and attention.

You can trade on interest rates directly by speculating at key times on whether interest rates will go up or down. This can be done with derivative products like spread betting and CFDs, and can be done on our platform.

However, speculating on interest rates is a complex and risky form of trading that comes with inherent potential loss. Also, both spread bets and CFDs are leveraged financial products. You would put down an initial deposit to open a larger position, with both profits and losses being calculated on the total position size. This means that leveraged products carry inherent risk of your losses or profits substantially outweighing your initial deposit.

Learn how to trade interest rate derivatives

Interest rates often have a knock-on effect on stocks, too. A lower interest rate could mean higher earnings from stocks, as businesses spend more in the more dovish environment. As people spend more on other things, so investors and traders spend more on stocks. This, in turn, can drive the price of those stocks up – which could drive the price of whole indices up, creating a virtuous circle where stock prices keep increasing.

The opposite can be said of a more hawkish environment. With many tightening their belts, including businesses and those buying or trading the stocks of those businesses, less money is spent. Enough people not buying or trading stocks can in turn drive the price of stocks down, both for individual companies and collectively.

Bonds, meanwhile, have a very different relationship to interest rates. Generally, when interest rates rise, bond prices fall and vice versa.

Because the amount of interest a bond can yield is partially affected by the interest rate, a lower interest rate will decrease the yield of a bond coming out now. However, there are always multiple bonds in circulation and a bond issued at the time of higher interest rate (thereby giving higher yield) will suddenly become more popular, further driving up that bond’s price due to its popularity.

In this way, lower interest rates drive down bond yields but can drive up bond prices – and the opposite is true for a higher interest rate.

FAQs

Who sets interest rates?

Interest rates are set at a national level by the central banks, which will inform the interest rates charged by lending institutions like local or regional banks. Interest rates are set at a national level by the central banks, which will inform the interest rates charged by lending institutions like local or regional banks.

How are interest rates calculated?

The central banks, like the Bank of England, set interest rates – but where do they get them from? In the UK, the Monetary Policy Committee (MPC) decides on the interest rate, led by a host of factors such as inflation levels (keeping the interest rate consistent with CPI) and what state the economy is in. Ultimately, lowering interest rates in tough times hopes to encourage consumer spending and saving to bolster flagging economies.

Banks and other lenders will then calculate their interest rates based off of the rate set by the MPC (called the bank rate in the UK) plus an additional amount on top in order to make a profit.

How can you work out how much interest you would earn?

As long as you know the rate at which you’re earning interest, you can figure out how much interest you’d earn. Take the amount in your savings or investment and multiply that by the interest rate percentage, then multiply that figure by the period of time the amount would be earning the interest for.

Say, for example, you have £1000 worth of savings, which is earning a 5% interest rate over a period of ten years. The total interest amount would be £500 (£1000 x 0.05 x 10).

How can you profit from interest rate changes?

You can make a profit (or loss) from the changes in interest rates in a number of ways.

Trade interest rates directly with us via spread bets or CFDs, where you can speculate on whether the interest rate will rise or fall.

Just remember that both are leveraged financial products, meaning that you’ll put down a small deposit to open a larger position, with both profits and losses calculated on the full trade size. This means that losses and profits can substantially outweigh your deposit amount, so always ensure you’re trading within your means.

Another way to take advantage of the interest rate is simply through saving or investing. When the interest rate goes up, so does your money’s potential to compound its interest and make you more savings over time.

Lastly, since the bond market has an inverse relationship to the interest rate, you can also invest or trade in bonds when you believe the interest rate will change. A rising interest rate means dropping bond prices and an interest rate cut usually means a rise in bond values.

Connect with us

Spread bets and CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% of retail investor accounts lose money when trading spread bets and CFDs with this provider. You should consider whether you understand how spread bets and CFDs work and whether you can afford to take the high risk of losing your money.

Professional clients trading spread bets and CFDs can lose more than they deposit.

The value of shares, ETFs and other ETPs bought through a share dealing account, a stocks and shares ISA or a SIPP can fall as well as rise, which could mean getting back less than you originally put in. Past performance is no guarantee of future results. Some ETPs carry additional risks depending on how they’re structured, investors should ensure they familiarise themselves with the differences before investing.

Crypto - Don’t invest unless you’re prepared to lose all the money you invest. This is a high-risk investment, and you should not expect to be protected if something goes wrong. Take 2 mins to learn more.

Share dealing and IG Smart Portfolio accounts provided by IG Trading and Investments Ltd, CFD accounts are provided by IG Markets Ltd, spread betting provided by IG Index Ltd, cryptoassets services are provided by IG Digital Assets Ltd.

IG is a trading name of IG Trading and Investments Ltd (a company registered in England and Wales under number 11628764), IG Markets Ltd (a company registered in England and Wales under number 04008957) and IG Index Ltd (a company registered in England and Wales under number 01190902). Registered address at Cannon Bridge House, 25 Dowgate Hill, London EC4R 2YA. IG Markets Ltd (Register number 195355), IG Trading and Investments Ltd (Register Number 944492) and IG Index Ltd (Register number 114059) are authorised and regulated by the Financial Conduct Authority.

The information on this site isn’t directed at residents of the United States, Belgium or any particular country outside the UK and isn’t intended for distribution to, or use by, any person in any country or jurisdiction where such distribution or use would be contrary to local law or regulation.