US jobs report preview: ADP and PMI hint at potential payrolls disappointment

Friday’s US jobs report could bring weaker outlook as ADP and PMI surveys hint at potential NFP disappointment.

The August US jobs report is due to be released at 1.30pm, on Friday 3 September (UK time). Coming off the back of a period which has been dominated by concerns over the timing of tapering, the trajectory of the US economy is as important as ever.

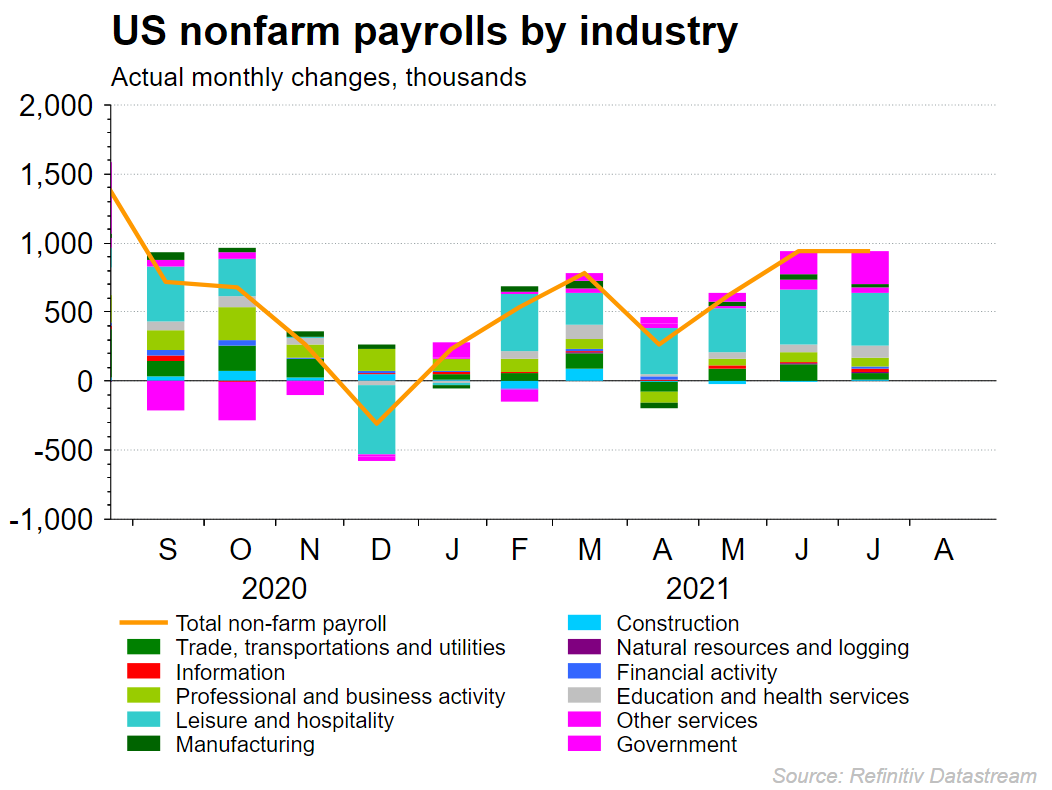

With that in mind, Friday’s jobs report provides us with a critical batch of information for both markets and the Federal Reserve (Fed) to consider in relation to monetary tightening. Last month saw an impressive 943,000 non-farm payrolls (NFP) figure, representing the best monthly rise in jobs for 11 months. Interestingly that also represents the third consecutive gain, and second consecutive month where the payrolls figure outperformed market estimates.

Unfortunately markets are expecting that recent upward trajectory to reverse this month, with economists forecasting a NFP figure of 750,000. The chart below highlights how the strong July jobs figure involved a significant government element once again, while leisure and hospitality continues to represent the biggest driver of job gains. With Delta Covid-19 cases on the rise, there will be some questions around just how long that services-sector rebound will remain strong.

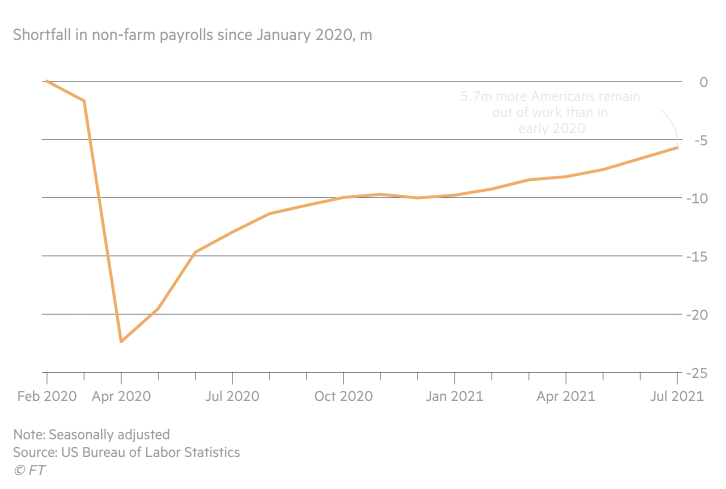

Ultimately, while we have seen significant improvements over the course of the past 17 months, a sizeable gap remains to get back to pre-Covid-19 pandemic levels. The chart below highlights how the US remains some 5.7 million jobs away from fully recovering.

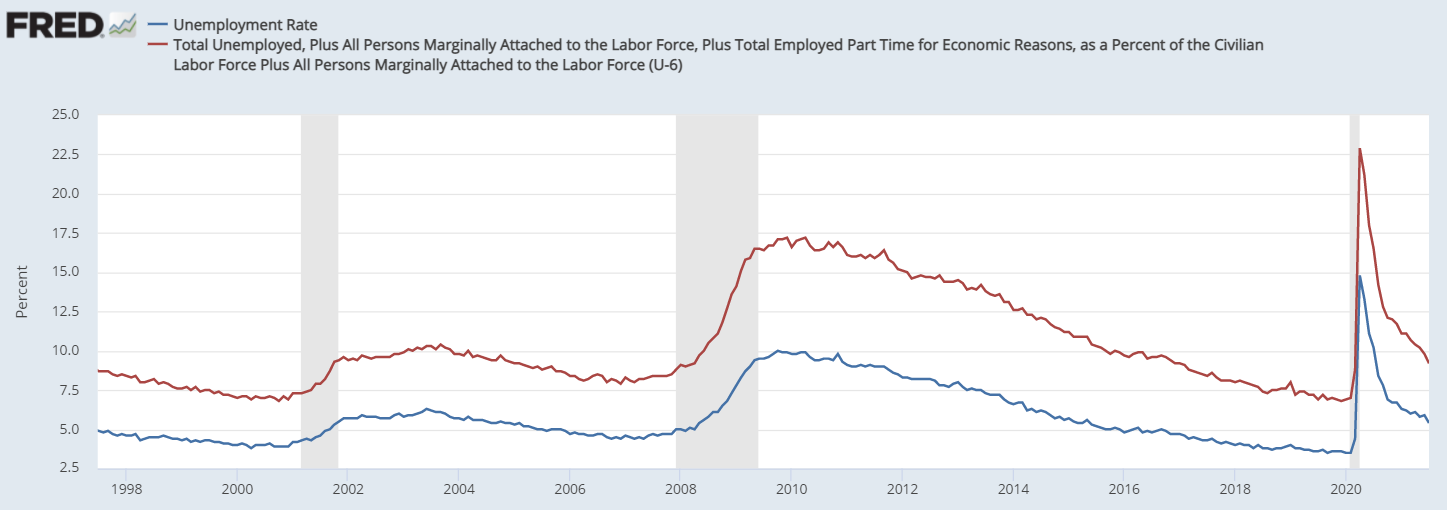

On the unemployment front, markets are expecting a continuation of the downward trajectory which has been evident throughout the past year. The rapid decline from 5.9% to 5.4% last time around is expected to be followed up with another move down to 5.3%.

However, the significant decline in participation rate does highlight how many unemployed individuals will simply have dropped out of the measure. As the economy recovers, those individuals will typically start to come back into the fold.

As such, it makes sense to also keep an eye out for the lesser-utilised U6 unemployment rate, which gives you a more widespread view of those out of work.

From an earnings perspective, markets are looking for the 4% year-on-year (YoY) average hourly earnings figure to remain steady. With inflation a key topic of note, the rate of earnings growth provides a key gauge of business costs going forward.

What do other employment readings tell us?

With the rising number of Delta variant cases and deaths in the US, there are fears that we could see the economic picture deteriorate as a result.

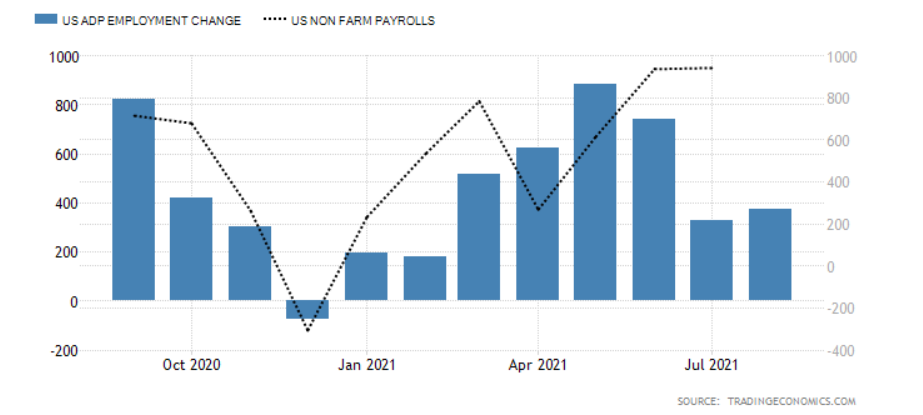

It is therefore useful to keep an eye out for what some of the other main employment readings say about the US jobs market right now. Automatic data processing (ADP) payrolls – the latest August ADP payrolls figure provided a worrying sign of what could be coming on Friday, with the figure of 374,000 falling well short of the 640,000 expected by markets.

It does represent an increase on the prior figure of 326,000, yet that prior reading was already significantly lower than the kind of job growth seen in the prior months. With that in mind, this does look like a potential reversal point for the headline NFP figure.

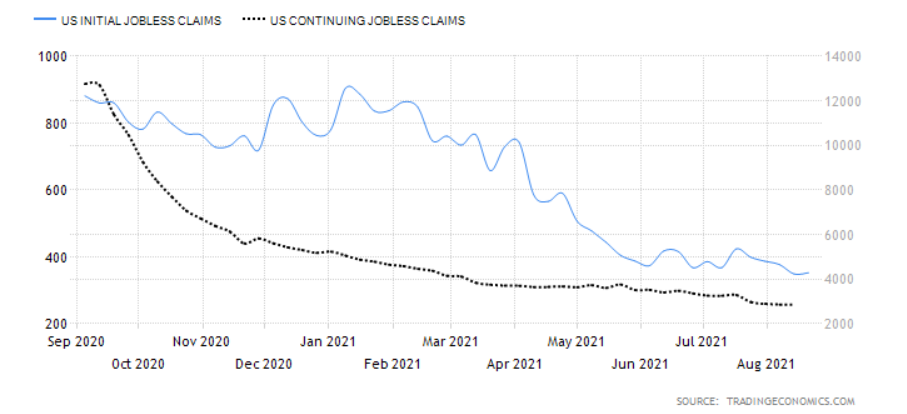

Jobless claims – both initial and continuing jobless claims have gradually drifted lower over the course of the recent months, with that trend continuing throughout August.

While there is little direct correlation that can be drawn between these figures and the payrolls reading, it does at least provide us with a good idea of whether we have seen a spike in joblessness which could impact Friday’s jobs figure.

Institute for supply management (ISM) manufacturing purchasing managers' index (PMI) – the latest manufacturing PMI reading from ISM did provide a positive move for the August survey. However, a closer look at the employment element of that survey has shown a sharp decline into contraction territory (49 from 52.9).

This provides yet another sign that we could see a significant move lower for payrolls on Friday, with the negative outlook for manufacturing employment indicated by purchasing managers bringing the potential for a weaker payrolls figure.

.png)

Dollar index technical analysis

The dollar has been on the back foot of late, with the index falling back into a confluence of 92.45 and 61.8% Fibonacci support.

There is a good chance we are looking at a retracement before we head higher, although we would need to see outperformance from the jobs report to help drive the dollar higher. Instead, with markets expecting a somewhat downbeat assessment of the economic recovery, we could see the dollar decline further in the event that such an event comes to fruition.

Near-term support comes into play at $92.23-$92.45, with a break below $91.77 required to bring a wider selloff into play.

S&P 500 technical analysis

The S&P 500 has conitued its steady climb higher, with the index reaching record highs on a habitual basis.

However, we are likely to see some form of pullback come into play before long, just like the move seen in mid-August.

In any case, the bullish outlook remains in play until we see the price fall back below the latest swing-low of 4352.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Be ready to act on the next non-farm payrolls report

Explore the influence the non-farm payrolls report has on American markets ahead of the next release on 2 July 2021.

Which markets could be more volatile after the NFP report?

Why was the report introduced and what does it tell us?

Why is the report important for traders?

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.