Key events to watch in the week ahead: 6 – 12 May 2024

What are some of the key events to watch next week?

This week’s overview

The Federal Reserve (Fed) meeting this week saw policy rate unchanged at 5.25%-5.50% in a widely expected move, but comments seem to lean slightly dovish. While the Fed noted a “lack of further progress” towards its inflation objective, the central bank reflected a high threshold for additional rate hikes despite the recent run in persistent inflation.

As a comfort to the broader risk environment, Fed Chair Jerome Powell saw rate hike as “unlikely”, while the central bank looked to slow its quantitative tightening (QT) process to a monthly run-off of $25 billion for Treasury securities from $60 billion.

Into the new week, here are five things on our radar.

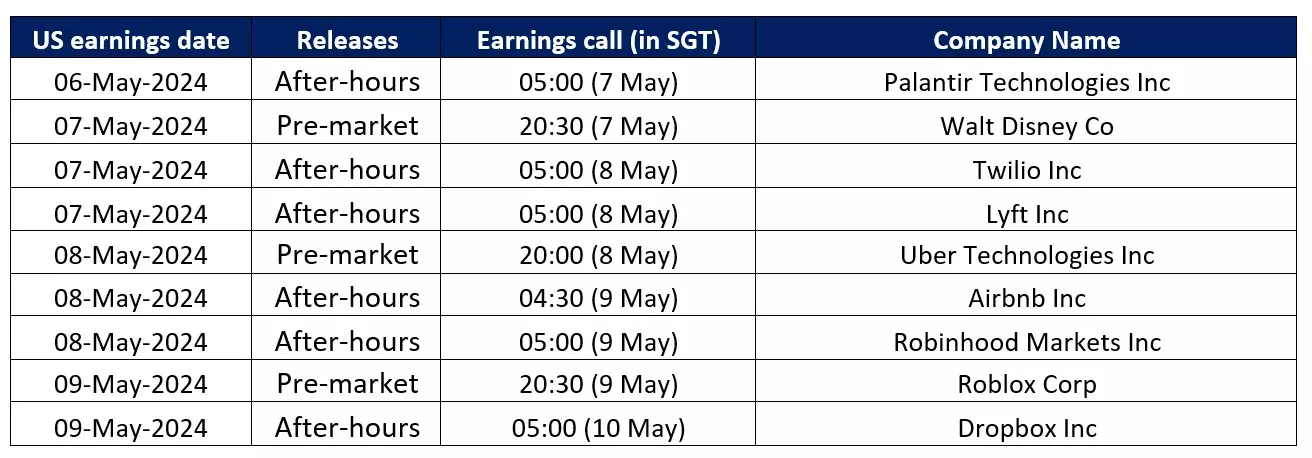

US earnings season: Palantir, Disney, Lyft, Uber, Airbnb, Robinhood, Roblox

With the big tech earnings behind us, the US earnings season may see some winding down over the coming weeks. Nevertheless, market participants will have their eyes on key earnings releases from Palantir, Disney, Lyft, Uber, Airbnb, Robinhood and Roblox.

Thus far, 78% of S&P 500 companies have reported their earnings, with 77% delivering an earnings beat. This is comparable to the outperformance rate seen in previous quarters, reflecting some resilience in corporate earnings.

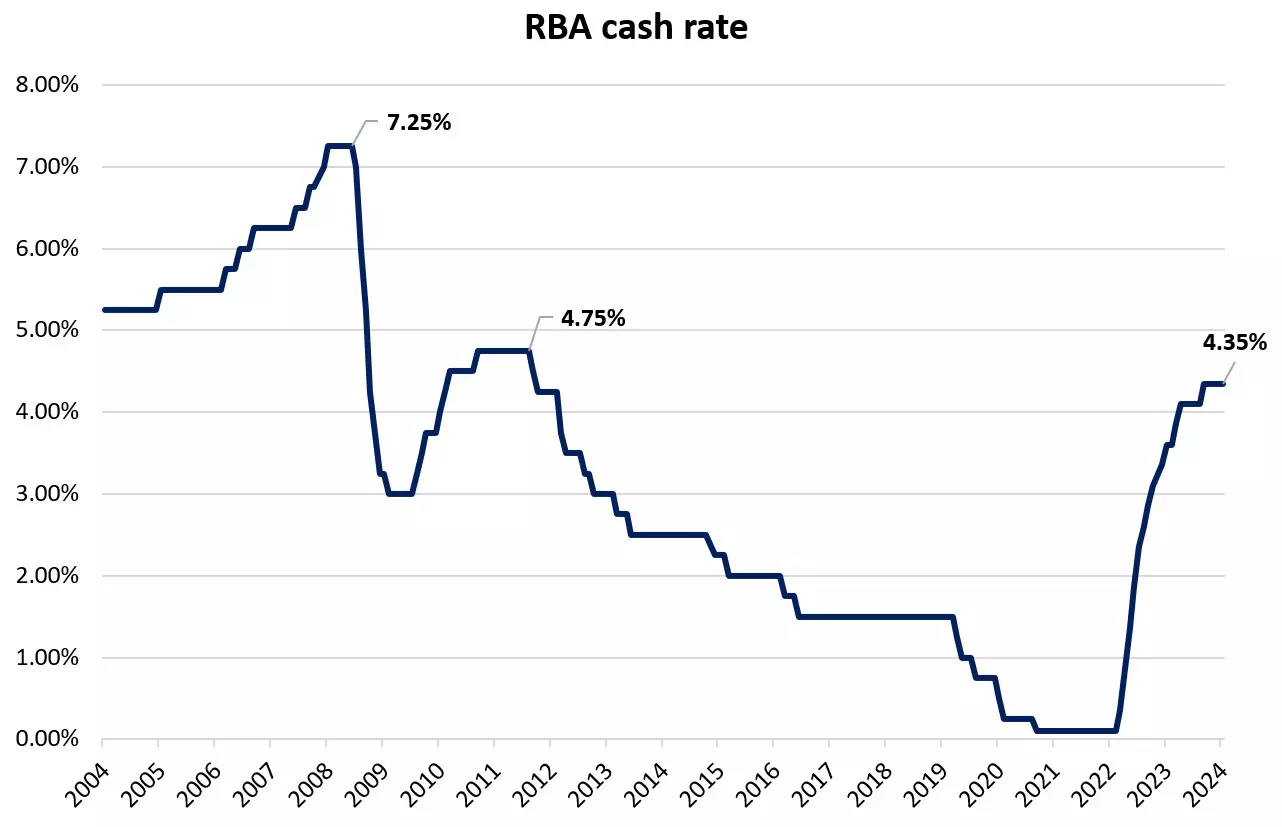

7 May 2024 (Tuesday, 12.30pm SGT): RBA interest rate decision

As widely expected, the Reserve Bank of Australia (RBA) kept its official cash rate on hold at 4.35% at its Board meeting in March.

The RBA noted that higher interest rates were working to establish a more sustainable balance between demand and supply. However, while goods inflation continues to moderate, it reiterated its concerns about sticky services inflation.

In the lead-up to the upcoming May Board meeting, firmer than expected Australian inflation and employment data has resulted in the Australian interest rate market swinging from pricing in RBA rate cuts this year to pricing in a 33% chance of a 25 basis point (bp) rate hike, before year-end.

While we view the bar to another RBA rate hike as very high, we acknowledge the window for rate cuts in 2024 has narrowed and have pushed back our call for a first RBA rate cut from August until November.

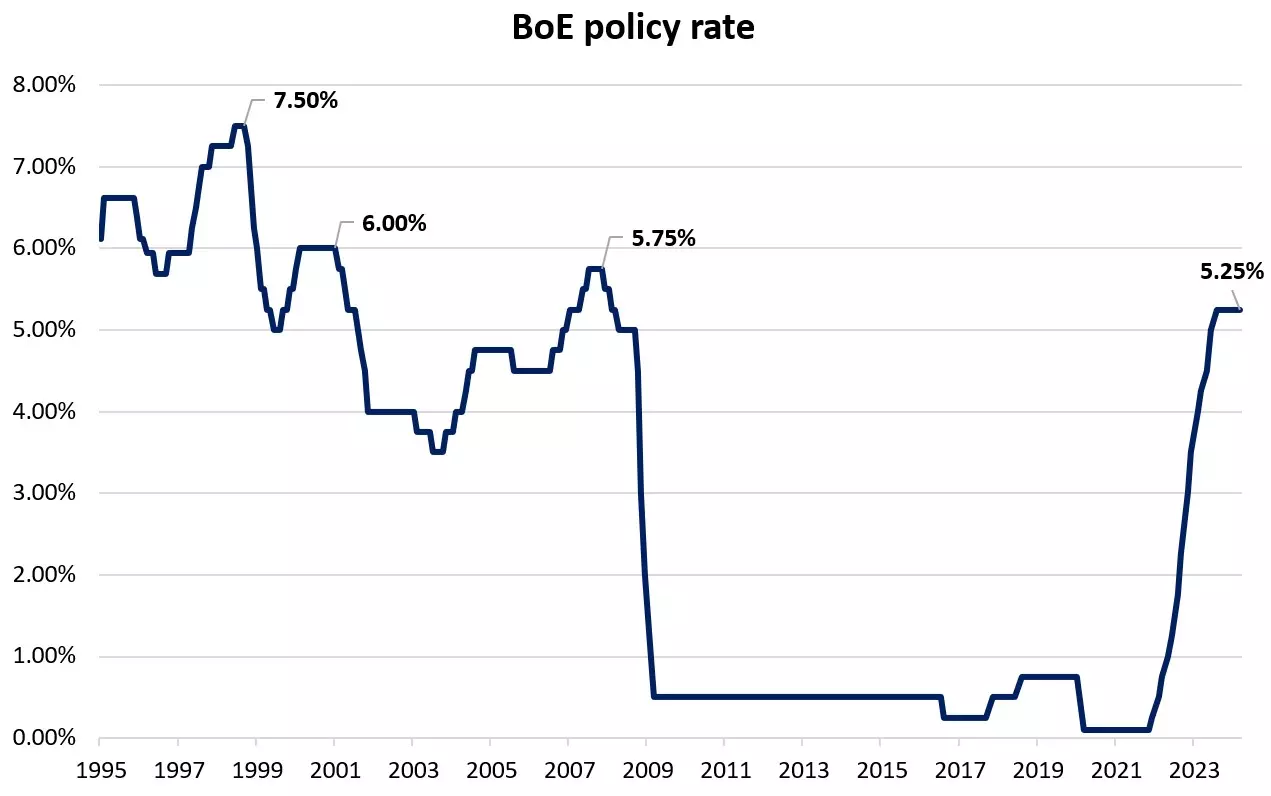

9 May 2024 (Thursday, 7pm SGT): BoE interest rate decision

As widely expected, the Bank of England (BoE) kept rates unchanged at 5.25% in March. However, the vote split provided a dovish surprise with an 8 - 1 vote as two members who had voted for hikes in February removed their hawkish dissent while a third continued to vote for a 25 bp ease.

There was no change to the forward guidance from February, when the BoE shifted to a neutral stance, with the BoE stating it "will therefore continue to monitor closely indications of persistent inflationary pressures and resilience in the economy as a whole, including a range of measures of the underlying tightness of labour market conditions, wage growth and services price inflation".

The announcement came a day after inflation data showed that country’s inflation rate had dropped to 3.4%, its lowest rate in almost two and half year’s. BoE Governor Bailey sound optimistic that condition were becoming more favourable for the central bank to consider rate cuts later this year. Ahead of this week meeting the UK rates market is pricing in at total of 44 bp of BoE rate cuts in 2024, with a first-rate cut fully priced for September.

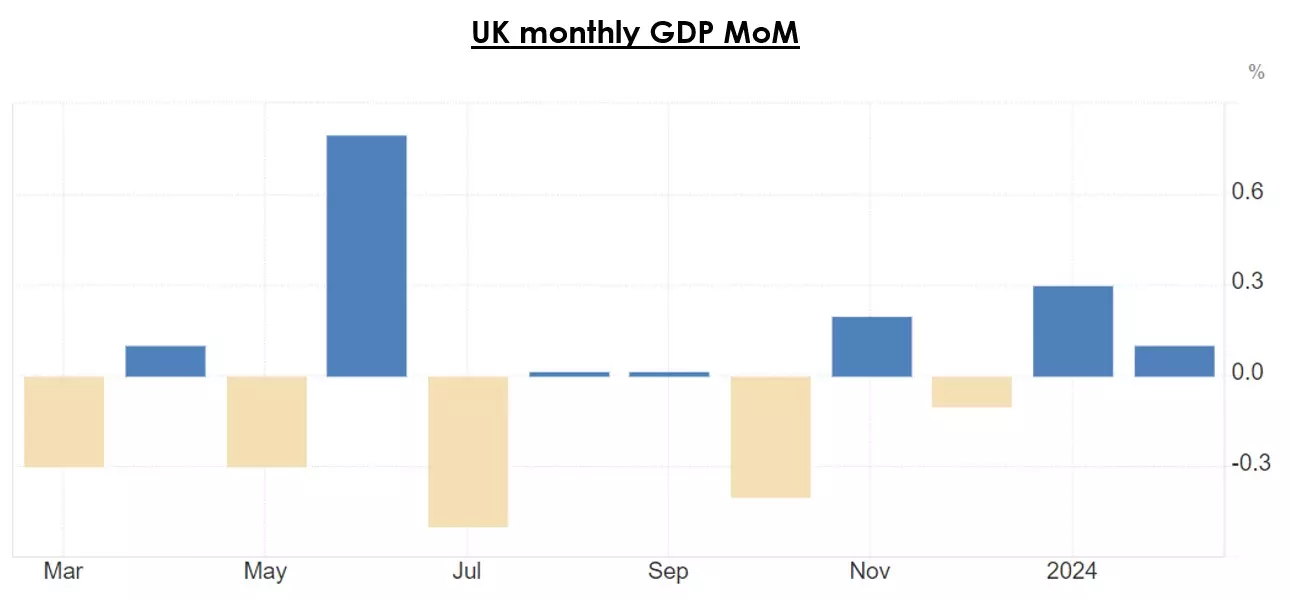

10 May 2024 (Friday, 2pm SGT): UK 1Q GDP growth rate

In February, the UK economy grew by 0.1% month-on-month (MoM), following a 0.2% growth in January. While overall growth remains sluggish, the readings show that the UK economy is on track to exit technical recession territory, after its economy contracted in the third and fourth quarter of 2023.

The release of the UK 1Q gross domestic product (GDP) next week may offer the confirmation that the recession has come to an end, and the economy could be starting to turn a corner. With UK’s inflation rate for March showing further easing to 3.2%, which is the lowest level since September 2021, market participants have been pricing for a rate cut from the BoE as early as August this year, potentially front-running the US Fed.

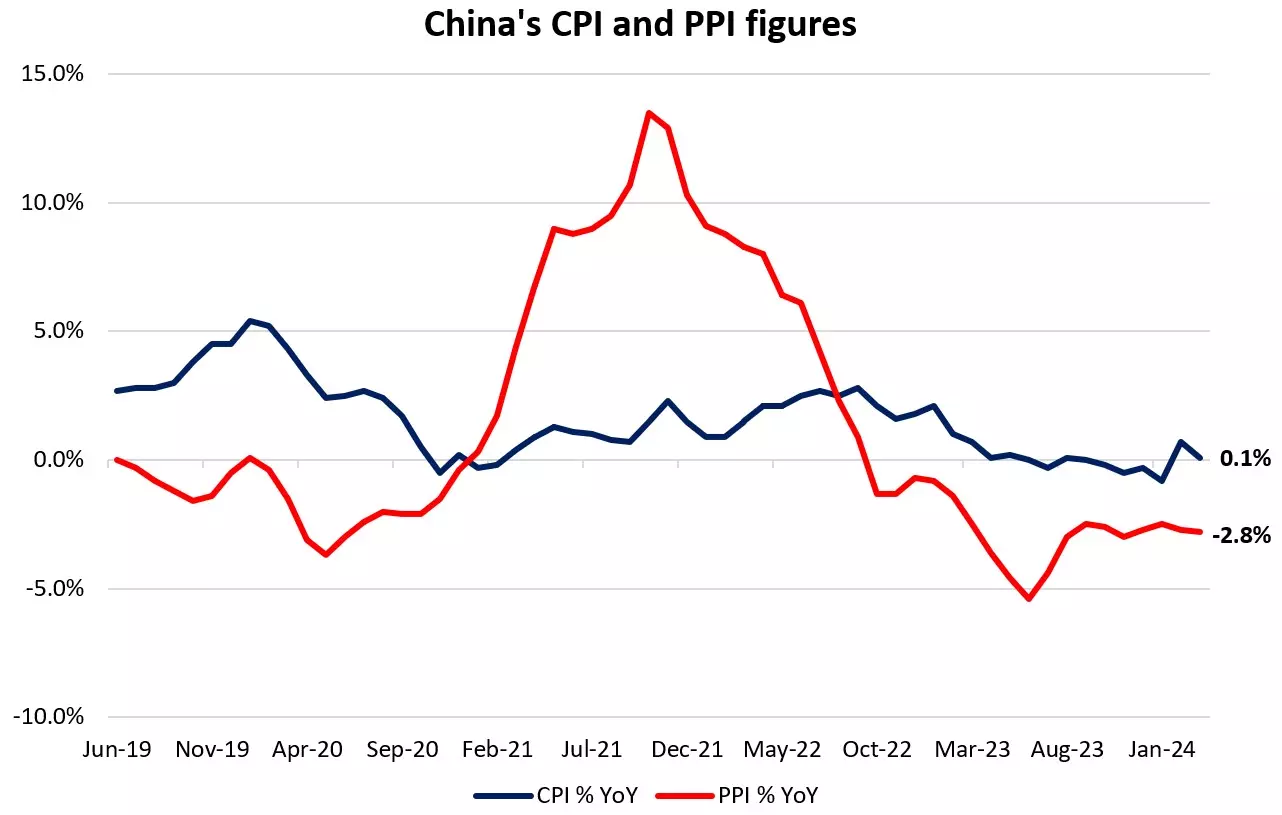

11 May 2024 (Saturday, 4pm SGT): China’s inflation rate

China’s consumer prices barely avoided deflationary territory in March, with its consumer price index (CPI) rising by just 0.1% year-on-year, down from the previous 0.7% as festive spending fades. March producer prices also weakened, with a deeper contraction at -2.8% versus the previous -2.5%.

While there are some green shoots emerging from China’s economic conditions, notably in the manufacturing sector, recovery has not been broad-based, with its services Purchasing Managers' Index (PMI) edging to its three-month low in April.

Ahead, expectations are for China’s consumer prices to improve to 0.3% year-on-year. Should there be any unexpected return to deflation for consumer prices, it may reinforce the still-weak domestic demand and raise calls for more supportive measure into the second half of this year.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.