Key events to watch in the week ahead: 8 - 14 April 2024

What are some of the key events to watch next week?

This week’s overview

The start of the second quarter was marked with a rough start for Wall Street, as market participants reconsidered their rate expectations, following a run in strong US economic data and mixed Fedspeak. Escalating geopolitical tensions in the Middle East also drove some near-term jitters, with concerns that oil prices at its five-month high may complicate the Federal Reserve (Fed)’s inflation right.

Into April, focus will be on the upcoming US earnings season to validate if the corporate earnings recovery since the second half of last year has further room to run. As usual, the earnings parade will kick off with the major US banks, with JPMorgan, Wells Fargo and Citigroup releasing their results next Friday.

Aside, here are four things on our radar.

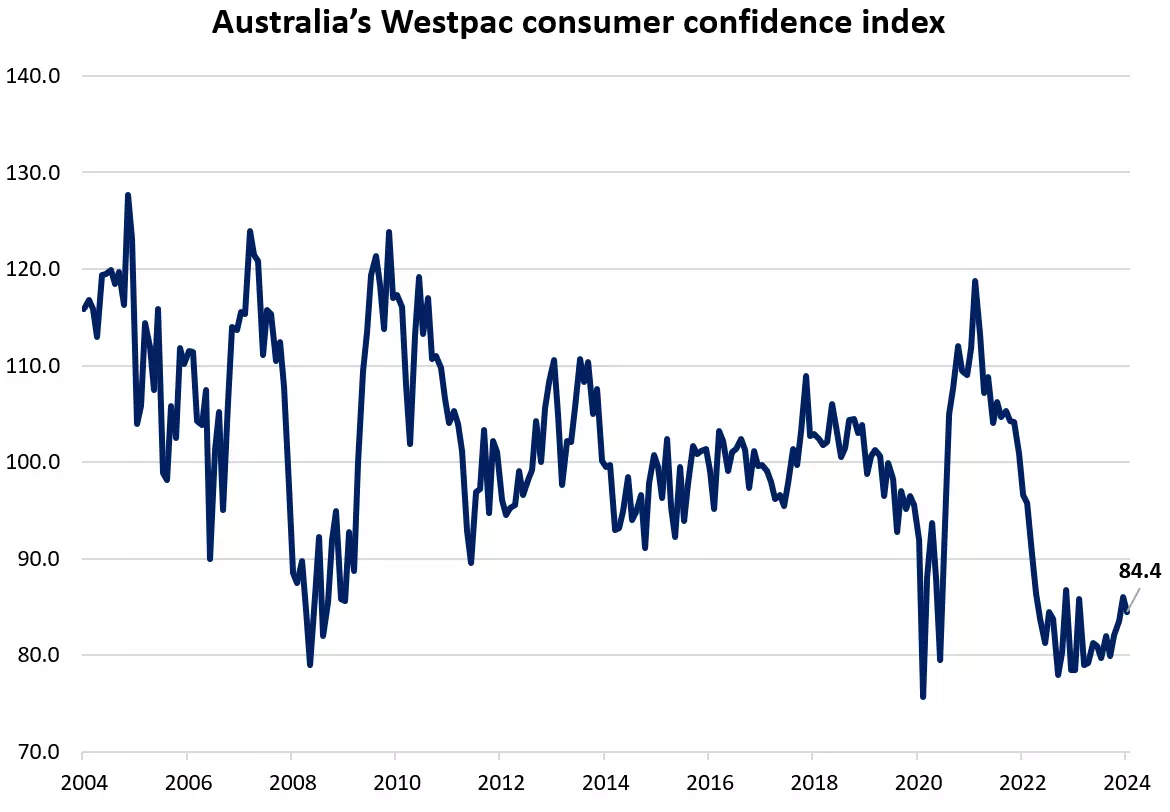

9 April 2024 (Tuesday, 8.30am SGT): Australia’s Westpac consumer confidence index

Last month (March), the Westpac Consumer Sentiment Index fell 1.8% to 84.4 from a 20-month high of 86 in February. The decline reflected ongoing pessimism from households concerned with their finances and cost-of-living pressures.

The recently released minutes from the Reserve Bank of Australia (RBA)’s March Board meeting showed that the RBA did not consider raising rates for the first time in nearly two years. The minutes' release coincided with the survey period for the Consumer Sentiment Index and should boost consumer confidence in April.

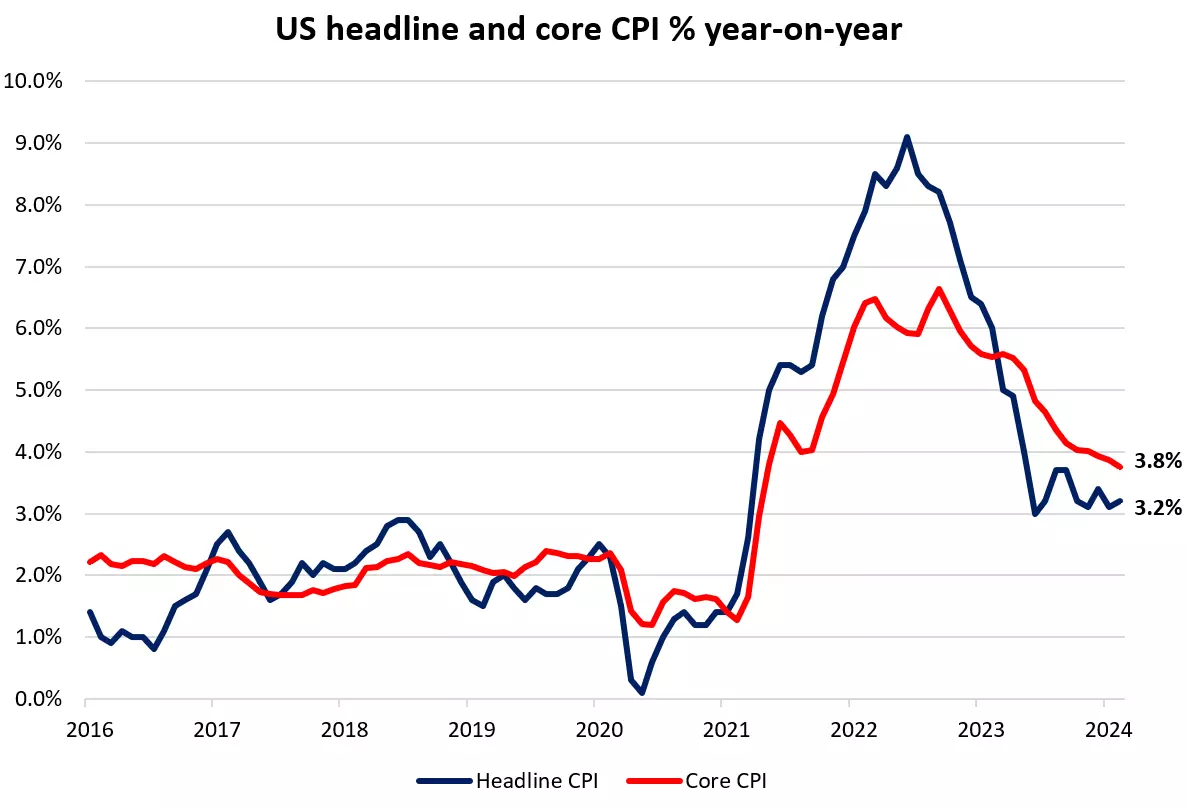

10 April 2024 (Wednesday, 8.30pm SGT): US CPI

In February this year, headline inflation in the US rose by 0.4% month-on-month (MoM), bringing the annual rate of inflation to 3.2%, above the 3.1% expected. Core consumer price index (CPI) also rose by 0.4% MoM, allowing the annual rate of core inflation to ease to 3.8% from 3.9% in January, but above market forecasts of 3.7%.

Although the headline and core inflation rates were higher than expected, within the details, there was a sharp normalisation in non-housing services inflation, and declines were observed in the super-core measure and the problematic owner’s equivalent rent category.

Further soothing nerves, Fed Chair Powell has reassured a number of times of late that despite hotter-than-expected inflation readings this year, inflation was on a “bumpy” road to 2% and that the central bank expects to lower rates at “some point” this year.

This month, the expectation is for headline CPI to rise by 0.4% MoM, which would see the annual rate climb to 3.5%. Core CPI is expected to rise by 0.3% MoM, which would see the annual rate cool to 3.7% from 3.8%.

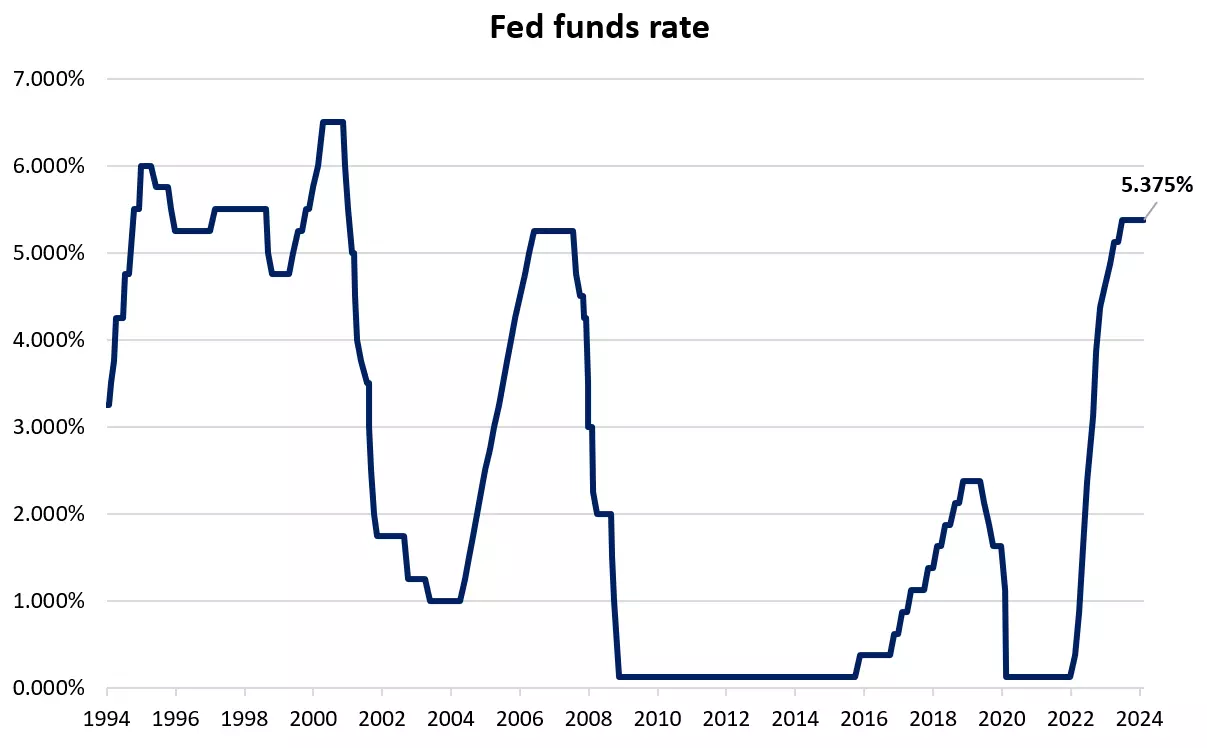

11 April 2024 (Thursday, 2am SGT): US Federal Open Market Committee (FOMC) meeting minutes

At its meeting in January, the Fed maintained its target rate for the Fed Funds at 5.25% - 5.50% for a fifth consecutive meeting, as widely expected. The Feds updated dot plots showed the median end 2024 dot remained at 4.625% and continued to show three 25 basis point (bp) rate cuts are expected this year.

The Fed revised its Personal Consumption Expenditures (PCE) inflation and growth projections higher for 2024. At the same time, its median unemployment rate was marked down to 4.0% in 2024 and maintained at 4.1% in 2025. The Fed Chair confirmed that an in-depth conversation had occurred about slowing the pace of balance sheet runoff, although a decision was not made on the size of the taper.

The minutes will be closely scrutinised for more details about the Fed's plans for its balance sheet, additional clues about when the Fed expects to start cutting rates, and its views on the run of hotter-than-expected US data.

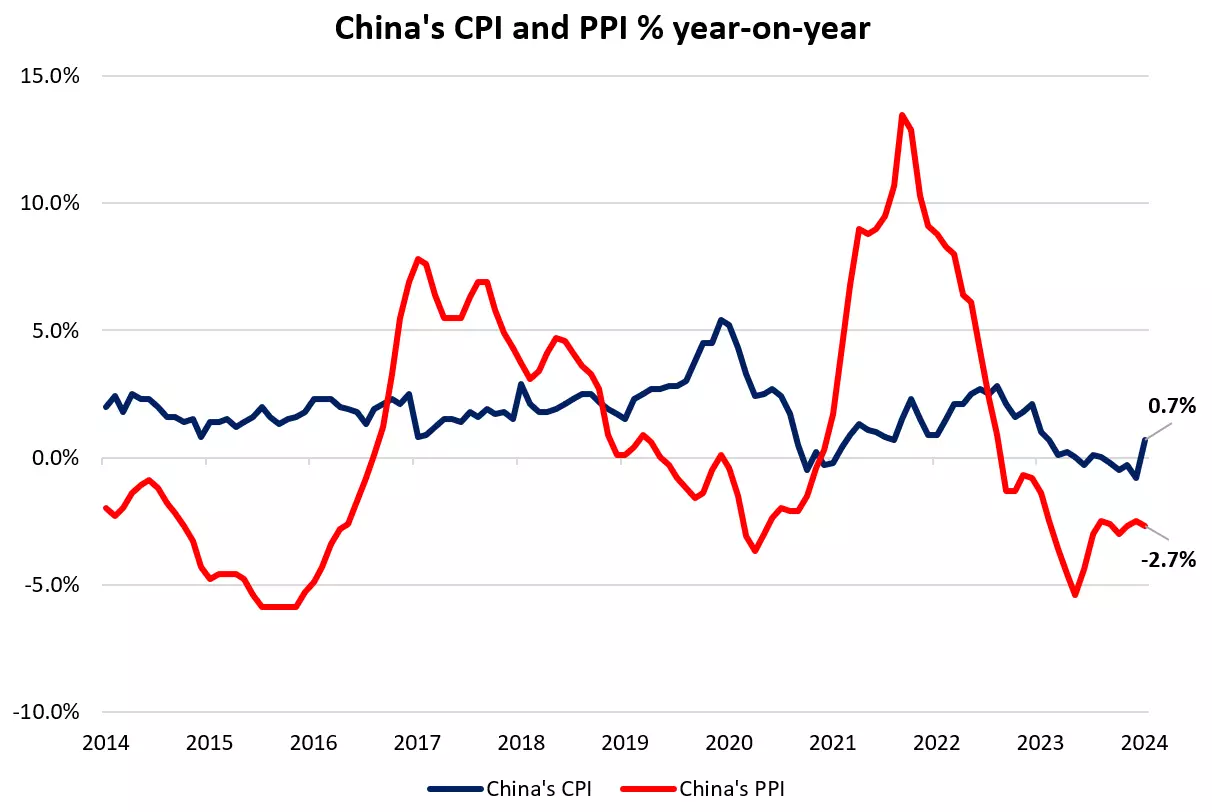

11 April 2024 (Thursday, 9.30am SGT): China CPI and producer price index (PPI)

China’s inflation data showed that consumer prices had reverted to positive territory in February with a 0.7% year-on-year growth, registering its first increase since September 2023. Its producer prices, however, remained subdued at a 2.7% year-on-year decline, which is a deeper contraction from the 2.5% decline in January.

With the turnaround in February consumer prices attributed to a spending boom during the Lunar New Year holidays from rising food prices to travel spend, all eyes will be on whether the surge in demand can be sustained or is just a one-off blip.

Upside surprises in China’s Purchasing Managers' Index (PMI) data this week offered some green shoots for China’s economic conditions, but any return to deflation ahead may easily dampen such optimism. For March, China’s consumer prices may ease to 0.4% year-on-year with lower food prices.

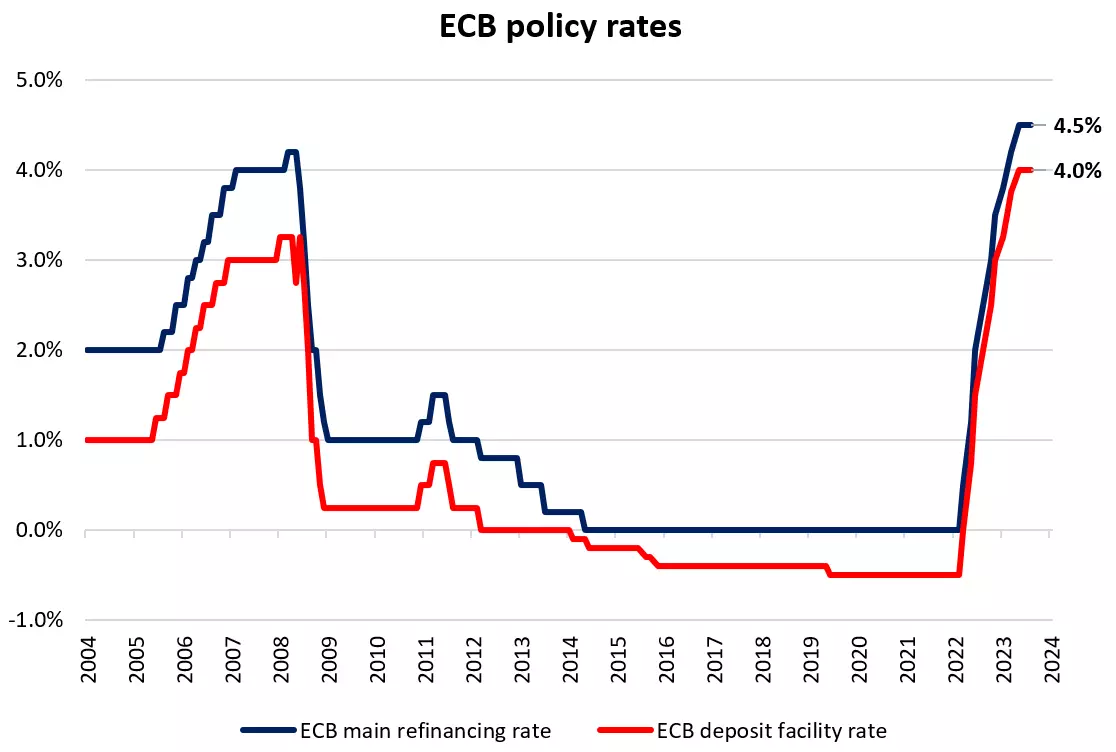

11 April 2024 (Thursday, 8.15pm SGT): ECB interest rate decision

Next week, the European Central Bank (ECB) is expected to keep interest rates unchanged for the fourth straight meeting, with its deposit facility rate at 4.0%. That said, with Eurozone’s inflation unexpectedly easing last month, the case for the ECB to kickstart its rate-cutting cycle as early as the June meeting has been strengthened.

The minutes of the March meeting revealed that policymakers have been laying the groundwork for imminent policy easing, stating that “the case for considering rate cuts was strengthening” and that the date of a first rate cut is now “coming more clearly into view.” Money markets are currently pricing an 80% probability for a June 25 bp rate cut and pencilling in three to four cuts by the end of the year.

While policymakers are unlikely to give the all-clear for the inflation fight just yet, any dovish shift in tone from the March meeting or hints of discussions on rate cuts at the upcoming meeting will be on watch to further provide validation for a policy move in June.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.