Key events to watch in the week ahead: 29 April - 5 May 2024

What are some of the key events to watch next week?

This week’s overview

Markets were faced with an onslaught of big tech earnings this week, which saw Meta share price taking a double-digit plunge, only for Microsoft and Alphabet’s earnings to provide Nasdaq with a lifeline thereafter.

Sentiments remain sensitive to the Federal reserve (Fed)’s policy outlook as well, as US economic data this week seems to put markets on a dilemma. The 1Q US gross domestic product (GDP) has weakened significantly to 1.6% quarter-on-quarter from previous 3.4%, but hopes for earlier rate cuts were dashed by persistence in pricing pressures, as reflected in the US Personal Consumption Price (PCE) Index.

Into the new week, here are five things on our radar.

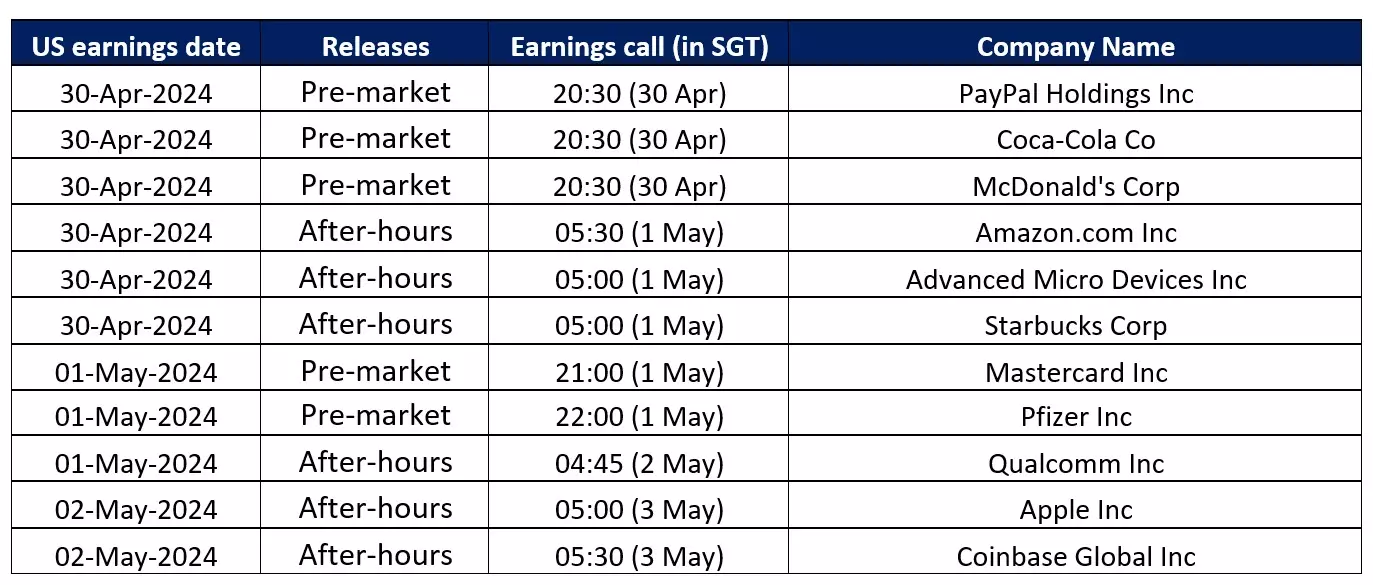

US earnings season: Amazon.com, Advanced Micro Devices, Starbucks, Qualcomm, Apple, Coinbase

Into the new week, market participants will continue to have their eyes on several earning releases from Amazon.com, Advanced Micro Devices, Apple, to see if the growth in tech sector can keep up with its valuation. Attention will also be on other key companies, such as Starbucks, McDonald's, Mastercard and Coinbase.

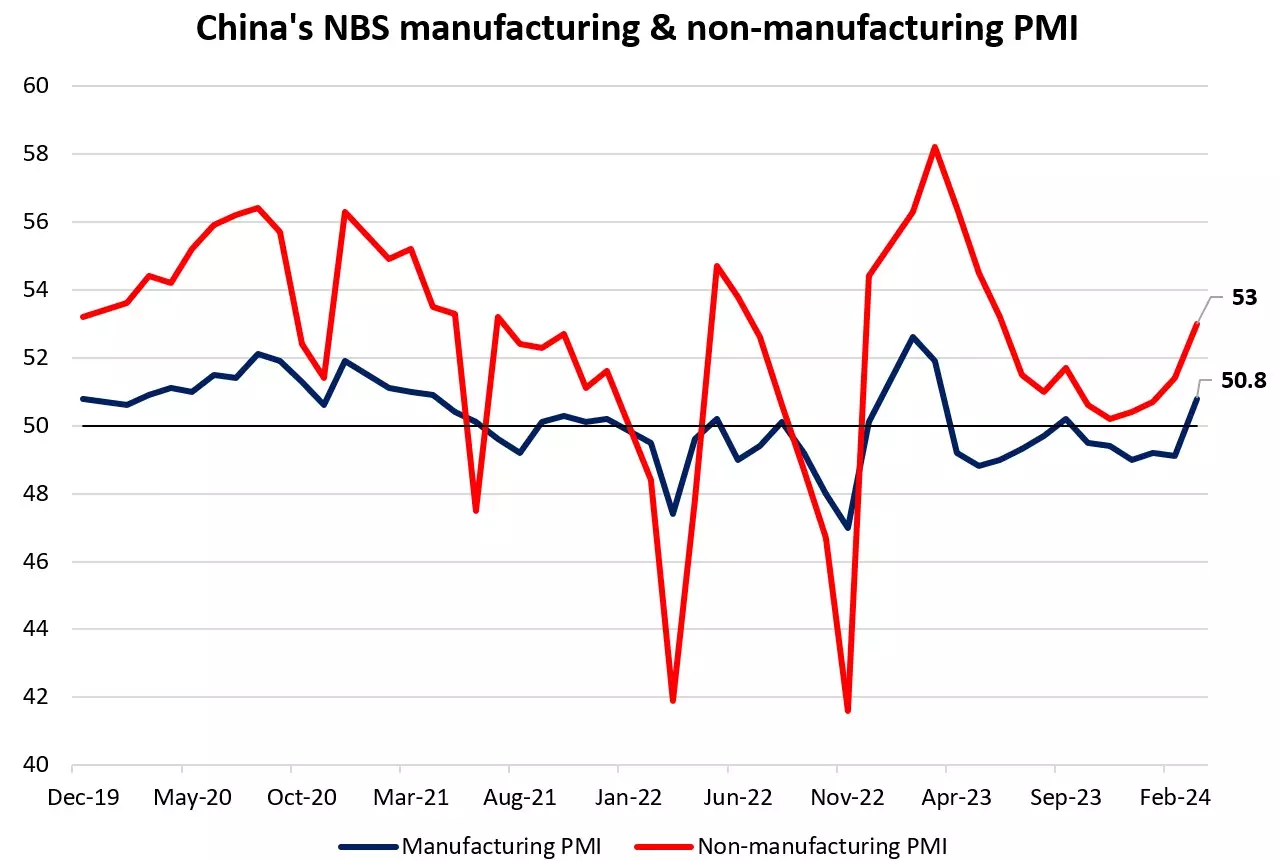

30 April 2024 (Tuesday, 9.30am SGT): China’s National Bureau of Statistics (NBS) manufacturing and services PMI

China’s March official Purchasing Managers' Index (PMI) figures have signalled some green shoots in its economy, with manufacturing activities returning to growth territory (50.8) after five consecutive months of contraction. Its non-manufacturing PMI has shown improvement as well, registering its highest level in nine months at 53.0.

Ahead, market participants will be watching if the recovery momentum will be durable, in order to reflect some degree of policy success and that the improvement is not only driven by seasonal factors. Ahead, expectations are for manufacturing activities to edge slightly higher to 51.2. Any fizzling out in growth momentum could like raise calls for policy support into the second half of this year.

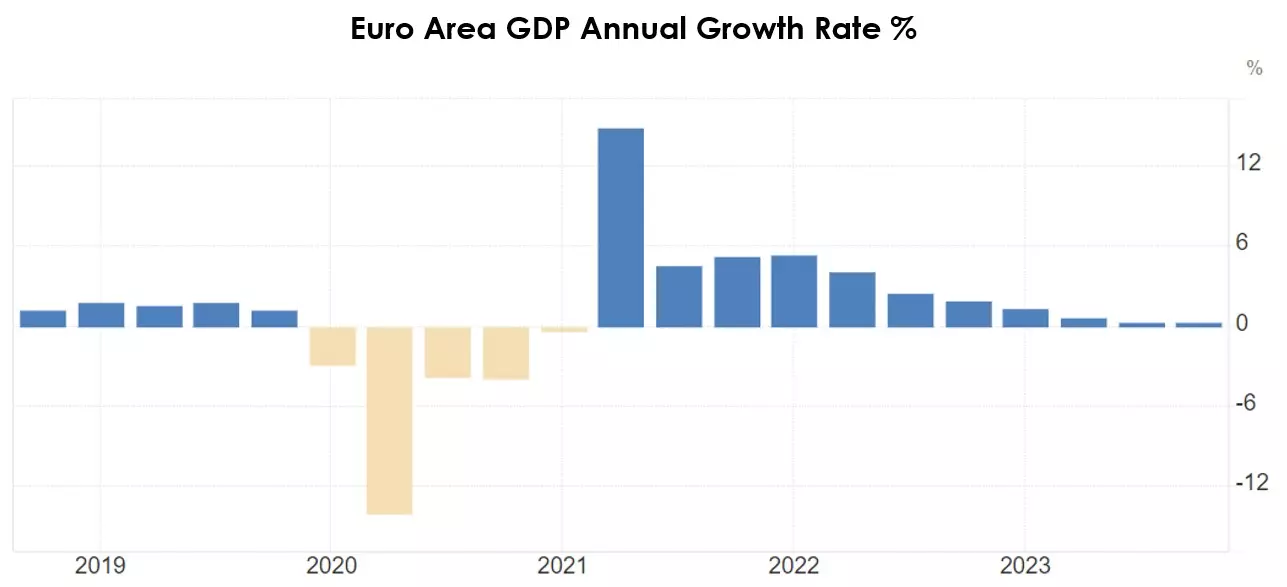

30 April 2024 (Tuesday, 5pm SGT): Euro area’s 1Q GDP

In the last quarter of 2023 (Q4 2023), the Eurozone unexpectedly avoided recession as firmer growth in Italy and Spain offset contraction in Germany for a growth rate of 0% following a 0.1% contraction in the third quarter.

Anaemic growth in the Eurozone during the second half of 2023 was due to elevated interest rates, high inflation, a slowing global economy and heightened geopolitical tensions.

In recent months, the European Central Bank (ECB) has acknowledged that inflation is on the right path to converge on its target and has signalled that it is expecting to ease monetary policy as early as June.

The prospect of imminent ECB interest rate cuts and a resilient global economy has resulted in a noticeable improvement in business surveys and PMI in the Eurozone. This improvement will also likely be viewed in the upcoming GDP release, with the market forecasting a rise of 0.5% quarter-on-quarter.

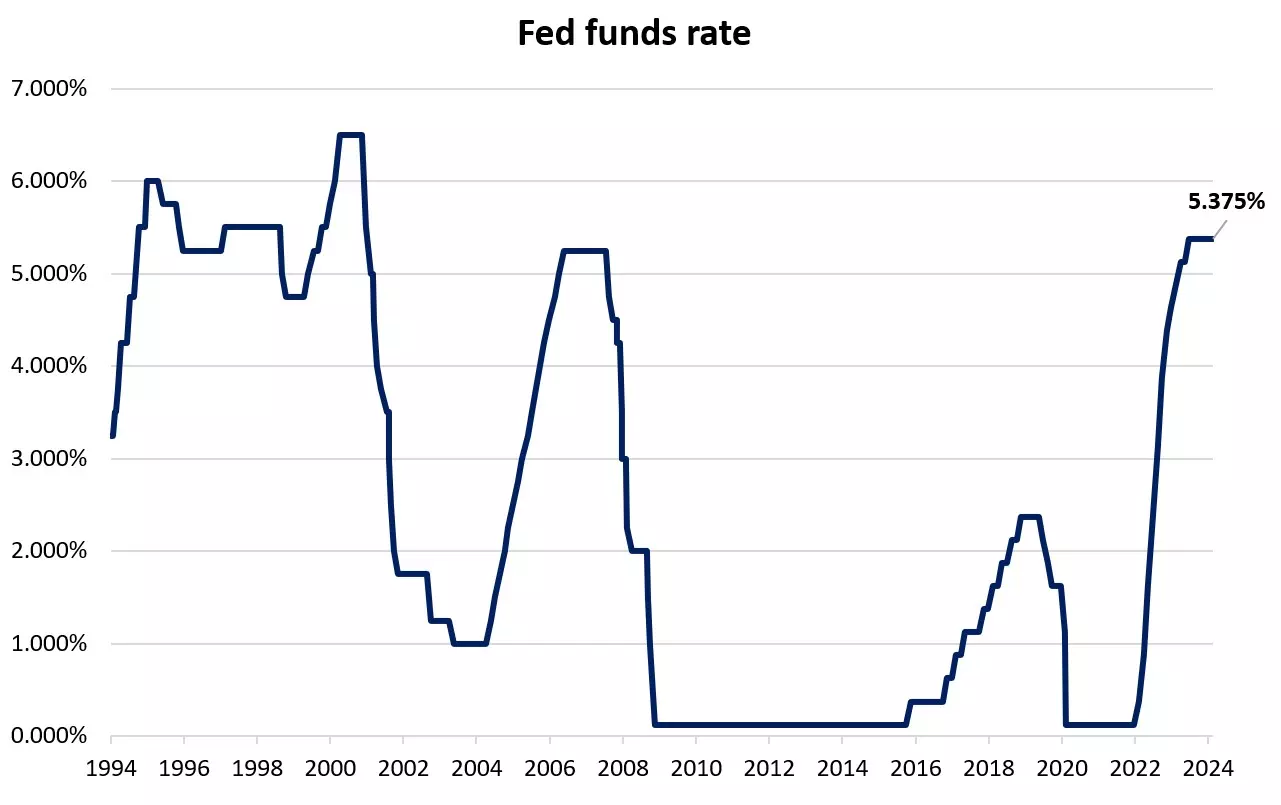

2 May 2024 (Thursday, 2am SGT): Federal Open Market Committee (FOMC) interest rate decision

In March, the FOMC kept the Fed Funds rate unchanged at 5.25%-5.50% for a fifth straight meeting. The accompanying statement was nearly identical to the January statement, reiterating that the Fed didn't expect to cut interest rates “until it has gained greater confidence that inflation is moving sustainably toward 2%.” The Fed's “Dot Plot” showed the median official was still expecting three 25 basis point (bp) rate cuts in 2024.

After the March FOMC meeting, the release of a third consecutive firmer-than-expected inflation report is expected to see the Fed keep rates on hold at 5.25%-5.50% in April and adopt a more hawkish tone in the press conference.

The Fed Chair will likely note the lack of progress on inflation and that the Fed will wait “longer than expected” to cut rates. The message of patience will likely be accompanied by an announcement that Balance Sheet tapering (QT) will begin in June by reducing the maximum monthly redemption cap on maturing securities from $60 billion to $30 billion.

The rates market is already pricing in a more hawkish outcome for the upcoming FOMC meeting, with a first-rate cut pushed back until December after the November US election.

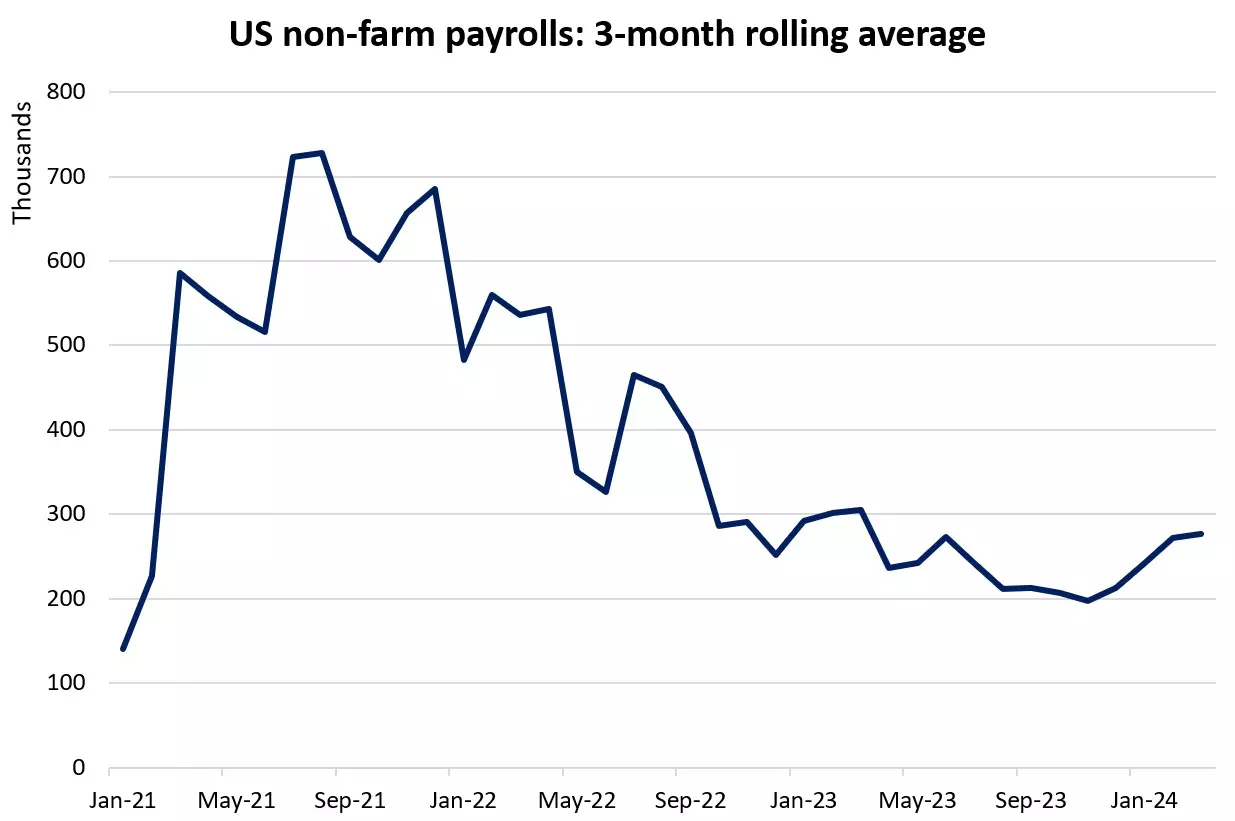

3 May 2024 (Friday, 8.30pm SGT): US non-farm payrolls

In his early-April comments, Fed Chair Jerome Powell has indicated some caution around the timing of rate cuts this year, reiterating that policymakers want to have greater confidence that US inflation is moving sustainably down to the Fed's 2% target. This comes as in his words, "recent readings on both job gains and inflation have come in higher than expected”.

Upside surprises in recent set of US inflation data have driven market expectations to lean towards having only one 25 bp rate cut from the Fed this year. This is pared down from the three rate cuts being priced just a month ago. Further strength in US labour conditions may likely reinforce views for the Fed to exercise more patience in its policy easing and rates to be kept high for longer.

Current consensus is for US to add 210,000 jobs in April, down from the previous 303,000 in March. With US job numbers pulling ahead of consensus for the past five months, markets will be watching if the trend may continue. Unemployment rate is expected to stay unchanged at 3.8% from March, while average wage growth is expected to stay unchanged as well at 0.3% month-on-month.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.