Can Tuesday’s US CPI reading stop the rout in global equity indices?

Can decent inflation data and optimism about the Fed's aid to banks lift market sentiment?

Is Tuesday’s lower inflation reading enough to stop the rout in equity indices?

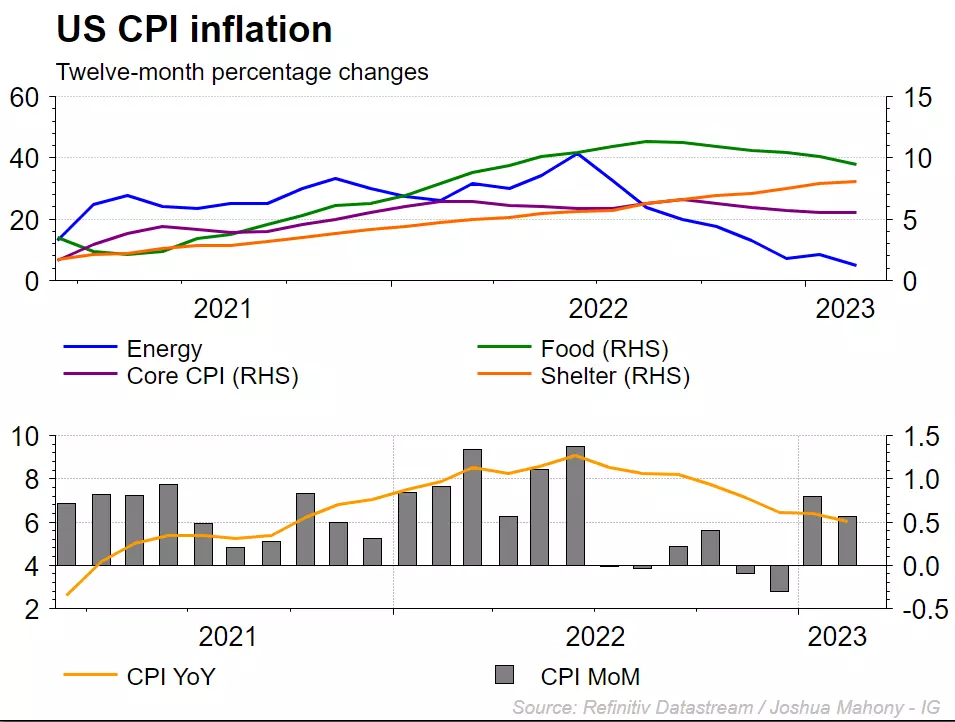

With the US annual Consumer Price Inflation (CPI) falling to 6% in February as expected and this being the lowest reading since September 2021, US equity indices got a boost on Tuesday and ended the day significantly higher, regaining some of their last few days’ sharp losses due to the collapse of Silicon Valley Bank (SVB).

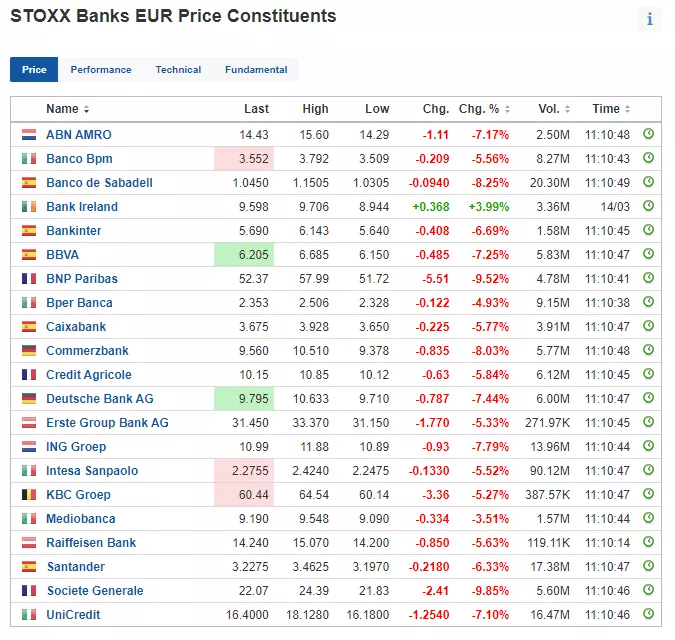

While European equity indices at first benefitted from the rally from their US counterparts, they resumed their descents on Wednesday morning due to ongoing worries regarding the impact rapidly rising interest rates may still have on European banks’ balance sheets with these again falling by on average over 5%, led by Credit Suisse’s over 20% drop.

STOXX Banks EUR Price Constituents

What about the US inflation picture?

Yes, there are signs that inflationary pressures are easing as a result of the Fed's tightening campaign over the past year with core inflation, which excludes food and energy prices, falling to 5.5%, the lowest level since late 2021, but these same rate hikes may have led to large bond portfolio losses for banks other than SVB if they didn’t hedge these appropriately, which was the top-20 US bank’s downfall.

The question thus is whether investors’ initial positive reaction to the latest US inflation data can be sustained or whether fear of the collapse of another bank may lead to sustained selling pressure and the resumption of the 2022 bear market.

The Labor Department's CPI report showed monthly inflation rose 0.4% in February from January, in line with expectations, resulting in a slowdown in annual inflation to 6%, the lowest since September 2021.

Even so, the same report showed that core inflation slightly exceeded expectations, underscoring a still challenging macro environment.

US CPI inflation

Investors have been speculating that the Fed may soon pause its tightening cycle as fears grow over the health of the broader financial system following the SVB bankruptcy and the closure of Signature Bank.

On the business side, US regional bank stocks regained ground after several tumultuous sessions, with First Republic Bank, for example, making back a large part of recently lost ground as the president of the bank declared to CNBC that he has not seen large capital outflows and that they have obtained additional liquidity after signing agreements with JPMorgan and the Federal Reserve (Fed). The stabilising action by the regulators has stopped the massive withdrawals of funds which has, at least for now, calmed the entire sector in the US.

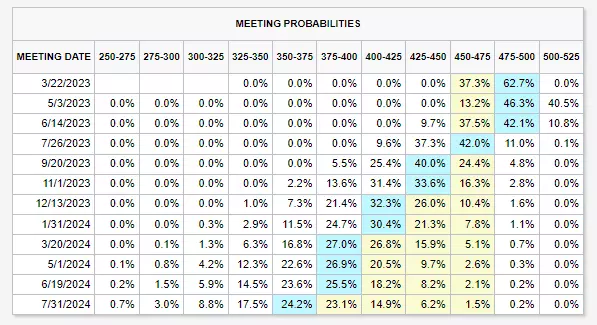

Furthermore, market bets have swung from a 70% probability of seeing a 50-basis point rate hike at next week’s FOMC policy meeting to a 37.3% chance of seeing no rate hike at all and a 62.7% change of seeing a 25-basis point hike.

US Fed meeting probabilities

With the European Central Bank (ECB) expected to disregard the current market woes and to remain solely focused on bringing inflation down to its 2% target, a 50-basis point rate hike to 3.5% may still be on the cards for Thursday’s monetary policy meeting, fuelling Wednesday’s banking sector sell-off and general risk-off sentiment.

The question is whether Wednesday’s rout in European equities will spill over to US markets or whether these can have a calming influence on their European peers.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Take a position on indices

Deal on the world’s major stock indices today.

- Trade the lowest Wall Street spreads on the market

- 1-point spread on the FTSE 100 and Germany 40

- The only provider to offer 24-hour pricing

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.