US non-farm payrolls preview – signs of slowdown in hiring and wage growth expected

This week’s payroll data may yet provide fresh hope to those expecting rate cuts in the first half of the year in the US.

Markets prepare for payrolls report as rate cut hopes fade

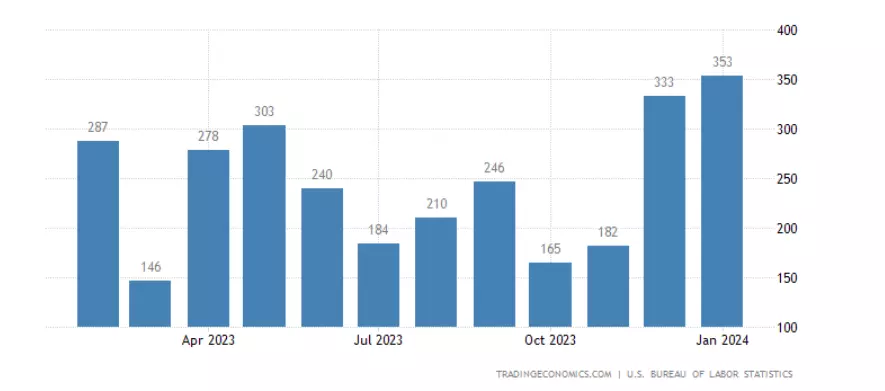

All eyes will be fixed on Friday's highly anticipated US labour market report for February, as traders search for clues on the likely trajectory of Federal Reserve (Fed) monetary policy in the months ahead. After a series of blockbuster job gains and stubbornly elevated wage growth readings, expectations are that this month's employment figures could finally show some moderation.

Economists polled by Reuters expect 200,000 jobs to have been created, with the unemployment rate to hold at 3.7%. Average hourly earnings, meanwhile, are expected to rise by 0.3% month-on-month (MoM) and 4.3% year-on-year (YoY).

If these figures come in as expected, the unemployment rate will have remained steady, but the payrolls number and wage figures will represent a slowdown from the previous month.

Rate cut hopes bolstered by cooling wage data and slower hiring

Markets are positioned for slower job creation and a deceleration in wage inflation based on the latest expectations data. Any clear signs of labour market cooling would likely be cheered by investors, as it would reinforce nascent hopes that the Fed could begin cutting interest rates later this year.

Markets rein in rate cut bets

The urgency for a potential Fed policy pivot has become more pronounced in recent weeks. As recently as late 2023, markets were pricing in a total of 160 basis points (bps) worth of rate cuts by the US central bank over the course of 2024. However, that aggressive easing outlook has been significantly pared back.

More recent futures market pricing indicates that rate cut expectations for 2024 have fallen to around just 80 bps of easing by the Fed. This repricing over the past two months has effectively brought market forecasts more in line with the Fed's latest guidance of around 75 bps worth of rate cuts spread across the year.

More inflation progress needed

The evolution of market expectations underscores the tight rope the Fed is walking as it weighs achieving an elusive "soft landing" by taming stubbornly high inflation without sparking a severe economic downturn. Policymakers have repeatedly stated that the path for future rate moves will remain data-dependent, particularly on clear evidence of progress on the inflation front.

As such, any loss of momentum in job creation and wage growth in the upcoming labour report could provide fodder for those anticipating a sooner-than-expected pivot towards rate cuts by the US central bank. On the other hand, signs that labour market tightness remains persistent would dampen prospects for an imminent change in the Fed's policy stance.

Given the heightened market sensitivity around the trajectories for inflation and interest rates, Friday's jobs figures are setting up to be a crucial data point. Traders and economists alike will be scouring the report for signs that could drive further adjustments in the expected pace and magnitude of Fed rate moves in 2024.

While a variety of factors remain in flux, one thing is clear: the US labour market holds the key for central bank deliberations and market positioning in the months ahead. In this charged environment, the upcoming employment data could mark a pivotal shift in fortunes for the Fed's hiking cycle and broader economic outlook.

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

See an opportunity to trade?

Go long or short on more than 17 000 markets with IG.

Trade CFDs on our award-winning platform, with low spreads on indices, shares, commodities and more.

Live prices on most popular markets

- Forex

- Shares

- Indices