Ahead of the game: July 17, 2023

Your weekly financial calendar for market insights and key economic indicators.

US equity markets surged, recovering all of last week’s losses and more, as investors cheered the release of a softer-than-expected June CPI report. The tech-heavy Nasdaq led the charge, surging above 15,500 for the first time in seventeen months. AI chip maker Nvidia was a standout, closing at a fresh all-time high.

Headline CPI in the US rose 0.2% in June, vs 0.3% expected, leading the annual rate to drop to 3.0% from 4%. Core CPI rose by 0.2% MoM, with the annual rate easing to 4.8%, the lowest since October 2021.

The impact of “base effects” (following Russia's invasion of Ukraine) made the fall more significant. The tailwinds of base effects, which have driven inflation lower in recent months, are set to become headwinds in the months ahead. Markets continue to fully price in a rate hike at the July FOMC to 5.25%-5.50%.

Locally, the ASX 200 rebounded spectacularly, rising by over 100 points on both Tuesday and Thursday following a stronger lead from Wall Street and as China announced increased support for its stagnating economy after soft inflation data sparked fears of deflation.

The other major local news was the Federal Government's announcement of the appointment of Michelle Bullock as the next Reserve Bank Governor of Australia, replacing the outgoing Governor Phillip Lowe. Michelle Bullock has been with the RBA since 1985 and will become Australia’s first female central bank governor.

Next week, the key events in Australia will be the RBA meeting minutes and the labour force report for June. China will report its Q2 GDP, with inflation reports in the UK and Japan. Q2 2023 earnings season gathers pace as well, with reports due to be released from companies including Bank of America, Morgan Stanley, Goldman Sachs, Tesla, and Netflix.

- Michelle Bullock named next Reserve Bank Governor of Australia, taking office on September 18

- Despite RBA's steady rates at 4.1%, Australian Westpac consumer confidence stays deeply pessimistic in July

- US headline CPI saw a lesser-than-expected rise of 0.2% in June, annual rate drops to 3.0% from 4%, while Core CPI grew by 0.2% MoM, annual rate at 4.8% from 5.3%

- US consumer inflation expectations ease to 3.8% in June from 4.1%, marking a third consecutive monthly fall

- After peaking at 5.12%, US 2-year yield retracts to 4.66%

- USD dollar index, the DXY, dips below critical support at 101.00/80

- Bitcoin hits a thirteen-month high of $31,818

- WTI Crude Oil leaps over 4.5% this week, topping $77.00 for the first time in eleven weeks

- USD/JPY drops over 2.9% to below 138.00, catalysed by lower US yields and messy unwinding of carry trades

- Gold ascends above $1960, a first in four weeks

- Chinese CPI disappoints at 0.0% vs expected 0.2%

- Wall Street's Volatility (VIX) index decreases 13.54% to 15.43.

- AU: RBA meeting minutes (Tuesday, July 18 at 11:30 am AEST)

- AU: Labour Force Report (Thursday, July 20 at 11:30 am AEST)

- CN: GDP (Monday, July 17 at 12:00 pm AEST)

- CN: IP, Retail Sales, FIA (Monday, July 17, at 12:00 pm AEST)

- CN: Loan Prime Rate (Thursday, July 20 at 11:15 am AEST)

- JP: Inflation (Friday, July 21 at 9:30 am AEST)

- US: Retail Sales (Tuesday, July 18 at 10:30 pm AEST)

- US: Industrial Production (Tuesday, July 18 at 10:30 pm AEST)

- US: Building Permits and Housing starts (Wednesday, July 19 at 10:30 pm AEST)

- US: Philadelphia Fed Manufacturing Index (Thursday, July 20 at 10:30 pm AEST)

- US: Existing Home Sales (Friday, July 21 at 12:00 am AEST)

- UK: Inflation (Wednesday, July 19 at 4:00 pm AEST)

- UK: Retail Sales (Friday, July 21 at 4:00 pm AEST)

Break down

-

Australia

RBA Meeting Minutes

Tuesday, July 18 at 1.10 pm AEST

The Minutes from the Reserve Bank's meeting in July are scheduled to be released on Tuesday, 20 July at 11.30 am. At its meeting in July, the RBA kept its cash rate on hold at 4.10%.

The RBA's decision to keep rates on hold was largely anticipated by the rates market (80% priced). In contrast, about two-thirds of the forecasting community predicted a rate hike.

The RBA's reasons for staying on hold echoed partly why it paused its rate hiking cycle in April - to assess the impact of a cumulative 400 basis points or rate hikes over the past fourteen months.

"Interest rates have been increased by 4 percentage points since May last year," and today's pause "will provide some time to assess the impact of the increase in interest rates to date and the economic outlook."

The RBA retained its tightening bias and noted that the most critical factors behind the next rate move would be "developments in the global economy, trends in household spending and the outlook for inflation and the labour market".

The Board meeting minutes would be expected to reiterate the sentiments outlined above. They will be closely scrutinised for clues about what other factors would prompt the RBA to act on its tightening bias and what factors might see the RBA extend the current pause in its rate hiking cycle.

After this week’s sharp repricing in the rates market, the probability of a 25 basis point rate hike from the RBA in August has fallen to just 23% this morning, with a full rate hike now not priced until December.

RBA cash rate chart

-

Australia

Labour force report

Thursday, July 20 at 11.30 am AEST

Last month (May), employment rose by 75.9k, far exceeding market forecasts for a rise of 15k. It was the largest monthly increase in employment since June 2022, which saw the unemployment rate fall back to 3.6%. The rebound in May followed a tepid rise of 4k jobs which saw the unemployment rate rise marginally to 3.7%.

This month (June), the market is looking for a +15k rise in employment and for the unemployment rate to remain stable at 3.6%. The participation rate is expected to remain unchanged at 66.9%, just below record highs.

AU Unemployment rate chart

-

UK

UK inflation

Wednesday, July 19 at 4.00 pm AEST

Last month headline inflation in the UK held steady at 8.7% YoY, above market expectations l for a fall to 8.4%. Alarmingly core inflation rose to 7.1% YoY, the highest since March 1992, and above market consensus for a rise of 6.8%.

This month (June), the market is looking for headline inflation to rise by 8.3% YoY from 8.7% in May. The UK rates market is pricing in 110p of rate hikes from the BoE over the next eight months, with a peak BoE terminal rate of 6.1% viewed in March next year.

After monthly GDP in the UK fell by -0.1% this week, it does underline the threat of stagflation for the UK economy, particularly if inflation fails to cooperate again this month.

UK inflation rate chart

-

CN

China GDP

Monday, July 17 at 12.00 pm AEST

A series of downside surprises in China’s economic data has led several major banks to cut their 2023 GDP growth forecasts for China to be between 5.1%-5.7%. While the broad estimates are still above the government’s GDP growth target of “around 5%” for the year, this is a significant downward revision from an earlier range of 5.5%-6.3%.

China’s 2Q GDP growth rate is expected to rise to 7.3% YoY in Q2, up from 4.5% in 1Q. While a stronger read may provide more conviction for its 5% GDP target to be achieved this year, it could also dampen some calls for policy support in the second half of this year. Nevertheless, with China’s economic surprise touching its lowest level since July 2021, some economic resilience may potentially be more well-received.

China’s GDP growth rate chart

-

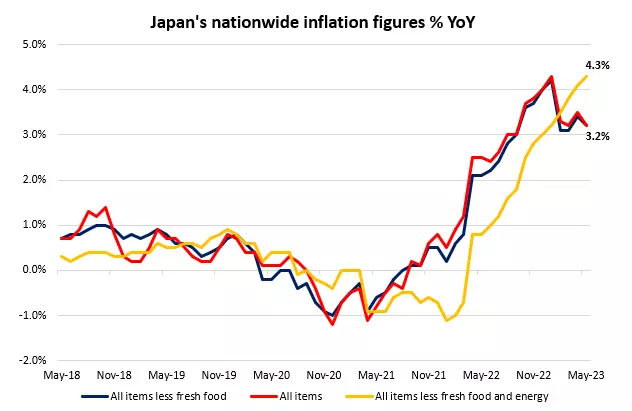

JP

Inflation

Friday, July 21 at 9.30 am

A recent pull-ahead in Japan’s wage pressures in May (2.5% versus 0.7% forecast) has challenged the Bank of Japan (BoJ)’s long-lasting view of inflation being ‘transitory’. In the aftermath of the data release, Japanese 10-year bond yields head higher, which reflects rising market bets for a quicker policy shift from the central bank, alongside a pick-up in the Japanese yen.

The next BoJ meeting lies just two weeks away, and with chatter that the central bank may tweak its yield curve controls sooner rather than later, the upcoming inflation data will be closely watched. Over the past four months, there has been a divergence between the “core core” aspect of inflation (less food and energy prices) against the headline figure.

Another pull-ahead in “core core” inflation this week (current 4.3%) will continue to widen the gap with the central bank’s 2% target, which may raise the odds of pricing pressures being more ingrained. That will likely support further hawkish positioning in the lead-up to the BoJ July meeting and provide further support to the Japanese yen in the near term.

Japan's inflation figures chart

-

US

US Q2 2023 earnings

With the S&P 500 closing at its highest level since April 2022, the upcoming earnings season will be on watch to justify whether corporate earnings are holding up amid the 500 basis-point (bp) worth of tightening from the Fed thus far. More notably, we will get a preview of big tech earnings from Netflix and Tesla.

For the second quarter, FactSet estimates suggest that S&P 500 earnings are expected to decline by 7.2%, which will be the third successive quarter of negative earnings growth and the largest earnings decline since Q2 2020.

Nevertheless, as seen in the last quarter, beaten-down earning expectations may also provide a lower hurdle for outperformance and room for positive surprises at a time when the US economic surprise index has touched its highest level since March 2021, just last week.

Companies’ forward guidance will be key as well. Amid the ongoing ‘earnings recession’, Refinitiv estimates are that Q2 will mark the bottom in earnings growth for the S&P 500, with recovery underway in Q3 and beyond.

US Q2 2023 earnings

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

Live prices on most popular markets

- Forex

- Shares

- Indices