Macro Intelligence: Where could the US economy land?

Will it be a soft, hard, or no landing?

What’s the ultimate destination for the US economy? In this week’s IG Macro Intelligence, we explore the three scenarios confronting the US: a soft landing, a hard landing, and a no landing.

Scenario 1: a soft landing

The US economy is proving resilient despite the historically rapid pace of monetary policy tightening. As inflation falls, but the economy continues to expand, the consensus view among market participants has shifted to a “soft landing” in the United States.

What is a soft landing?

A soft landing can be broadly defined as a scenario where interest rates are hiked and inflation falls, but the slowdown in economic activity and job losses are only mild.

A soft landing doesn’t necessarily mean avoiding a recession. However, any recession would be mild, and the economy would return to a steady expansion afterward.

What are the odds of a soft landing?

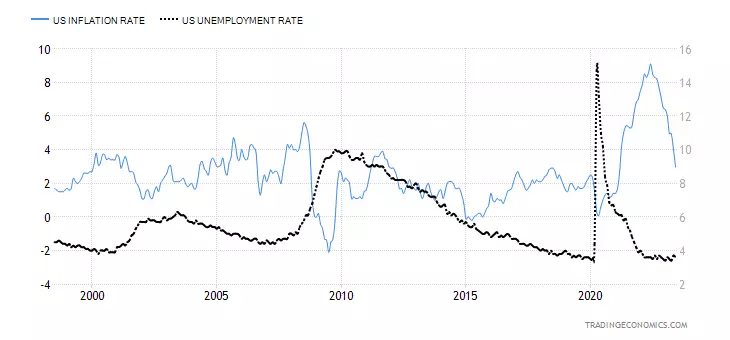

Following recent CPI data, which revealed inflation is falling towards the Fed’s target faster than previously thought possible, along with continued strength in the US labour market, markets are pricing in reasonable odds of a soft landing.

The headline inflation rate was 3% in June, while the unemployment rate remains at 3.6% and near multi-decade lows.

US inflation rate vs US unemployment rate

The US equity market appears to be pricing in a soft landing, with S&P 500 earnings expected to expand going forward and at an especially healthy rate in the calendar year 2024.

If a soft landing materialises for the US economy, it would likely be supportive of risk assets, such as equities. Although a recession does impact earnings growth, arguably, the S&P 500 has already experienced this contraction, following two quarters of negative profits in Q4 22 and Q1 23, with a likely third in a row this quarter.

US 500 cash weekly chart

Scenario 2: A hard landing

Though US fundamentals remain robust, some argue that given the "long and variable lags" of interest rate increases, the effects of unprecedentedly rapid policy tightening have yet to fully manifest.

What is a hard landing?

A hard landing is characterised by a sudden and severe recession in response to aggressive monetary policy tightening. While inflation would likely return to target quite rapidly, growth would contract substantially, leading to significant job losses.

In this scenario, the US economy would undergo a "technical recession", defined as two consecutive quarters of negative GDP growth. More critically, this would justify a decision by the National Bureau of Economic Research to declare an "official" recession.

What are the odds of a hard landing?

Considering the recent series of strong economic numbers and moderating inflation, the odds of a hard landing have arguably lessened. Despite this, there are some indicators of an impending, profound recession – and history suggests that it is a likely outcome.

The US yield curve is deeply inverted, with the spread between the 10-year and 2-year yield recently falling to its lowest point in four decades.

US yield curve chart

The ISM Manufacturing Index also suggests that the US economy is nosediving toward a recession. Although, resilience in services activity, mostly as consumers continue to spend significant savings buffers, could counter this downturn.

ISM manufacturing index

How will markets respond to a hard landing?

Given that markets are expecting a soft landing for the US economy, a rapid slowdown in growth could come as a nasty shock. US equities would fall as earnings expectations readjust. Growth-sensitive commodities, such as oil, copper, and iron ore, would reverse.

A recession would lead to aggressive interest rate cuts from the US Federal Reserve to support the economy. Yields would subsequently tumble, boosting the price of gold.

The most significant downside risk could materialise in yen crosses. Although the USD/JPY (大口) could rise if any slowdown resulted in financial stress, high-beta crosses like the AUD/JPY would fall as volatility spikes, yields drop, and commodity prices fall.

AUD/JPY weekly chart

Scenario 3: A no landing

The latest spate of strong US data has sparked the re-emergence of the so-called "no landing" scenario for the economy.

What is a no landing?

Although counterintuitive, a no landing scenario would see inflation fall, and the US economy re-accelerate and avoid recession. It is the polar opposite of a hard landing and is different from a soft landing because it suggests that growth will pick up going forward without exacerbating inflation pressures and inviting even more aggressive policy from the US Federal Reserve.

What are the odds of a no landing?

A "no landing" is improbable, with many commentators suggesting that the phrase itself is nonsensical. No hard indicators signal that such an outcome is unfolding, and the scenario relies on an imminent return of both headline and core inflation to target, not to mention steady employment growth and a greater expansion in corporate profits.

A no landing scenario would also require the pricing out of the slight easing implied in the rates curve, which itself could inspire a rotation in equity markets towards more cyclical assets, reversing the year's outperformance of growth stocks over value stocks.

How will markets respond to a no-landing?

A no-landing scenario in the United States would be the most bullish for markets and would spur further strength in equities. The rally would drive a broader rally for the S&P 500 while the cyclical Dow Jones and Russell 2000 would experience outperformance.

Commodity prices would rise from a weaker US dollar, and oil, copper, and iron ore would lift as economic activity improves. That would be a major tailwind for the AUD/USD and other high beta-currencies.

Russell 2000 weekly chart

This information has been prepared by IG, a trading name of IG Australia Pty Ltd. In addition to the disclaimer below, the material on this page does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. IG accepts no responsibility for any use that may be made of these comments and for any consequences that result. No representation or warranty is given as to the accuracy or completeness of this information. Consequently any person acting on it does so entirely at their own risk. Any research provided does not have regard to the specific investment objectives, financial situation and needs of any specific person who may receive it. It has not been prepared in accordance with legal requirements designed to promote the independence of investment research and as such is considered to be a marketing communication. Although we are not specifically constrained from dealing ahead of our recommendations we do not seek to take advantage of them before they are provided to our clients.

Live prices on most popular markets

- Forex

- Shares

- Indices