Key events to watch in the week ahead: 17-21 July 2023

What are some of the key events to watch next week?

This week’s overview

It has been a risk-on week, as downside surprises in US inflation offered room for the Federal Reserve (Fed) to conclude its hiking cycle sooner rather than later. The S&P 500 has touched its highest level since April 2022, driven by another pull-ahead in rate-sensitive growth sectors once more.

Heading into the new week, here are five key events to watch:

US 2Q earnings season: Bank of America, Goldman Sachs, Netflix, Tesla

With the S&P 500 closing at its highest level since April 2022, the upcoming earnings season will be on watch to justify whether corporate earnings are holding up amid the 500 basis-point (bp) worth of tightening from the Fed thus far. More notably, we will get a preview of big tech earnings from Netflix and Tesla.

For the second quarter, FactSet estimates suggest that S&P 500 earnings are expected to decline by 7.2%, which will be the third successive quarter of negative earnings growth and largest earnings decline since Q2 2020. Nevertheless, as seen in the last quarter, beaten-down earning expectations may also provide a lower hurdle for outperformance and room for positive surprises, at a time when the US economic surprise index has touched its highest level since March 2021 just last week.

Companies’ forward guidance will be key as well. Amid the ongoing ‘earnings recession’, Refinitiv estimates are that Q2 will mark the bottom in earnings growth for the S&P 500, with recovery underway in Q3 and beyond. Therefore, companies’ outlook will be key in validating such views on whether the worst in corporate earnings may be behind us.

17 July 2023 (Monday, 10.00am SGT): China’s 2Q gross domestic product (GDP)

A series of downside surprises in China’s economic data has led several major banks to cut their 2023 GDP growth forecasts for China to be between 5.1%-5.7%. While the broad estimates are still above the government’s GDP growth target of “around 5%” for the year, this is a significant downward revision from an earlier range of 5.5%-6.3%.

Current expectations are for China’s 2Q GDP growth rate to turn in a 7.3% growth year-on-year, up from the 4.5% in 1Q. Quarter-on-quarter, a 0.5% growth is the consensus, which may reflect a more tepid growth from the 2.2% in 1Q.

While a stronger read may provide more conviction for its 5% GDP target to be achieved this year, it could also dampen some calls for policy support in the second half of this year. Nevertheless, with the China’s economic surprise touching its lowest level since July 2021, some economic resilience may potentially be more well-received.

A series of key economic data will be released alongside as well, such as retail sales (est 3.2% versus 12.7% in June), industrial production (est 2.6% versus 3.5% in June) and fixed asset investment (3.5% versus 4% in June).

18 July 2023 (Tuesday, 9.30am SGT): Reserve Bank of Australia (RBA) meeting minutes

The RBA has kept its cash rate on hold at 4.10% at its July meeting, indicating their intent for some wait-and-see to assess the impact of the cumulative 400bp of rate hikes thus far.

Nevertheless, the RBA retained its tightening bias and noted that the most critical factors behind the next rate move would be "developments in the global economy, trends in household spending and the outlook for inflation and the labour market".

The Board meeting minutes would be expected to reiterate the sentiments outlined above. They will be closely scrutinised for clues about what other factors would prompt the RBA to act on its tightening bias and what factors might see the RBA extend the current pause in its rate hiking cycle.

After this week’s sharp repricing in the rates market, the probability of a 25bp rate hike from the RBA in August has fallen to just 23% this morning, with a full rate hike now not priced until December.

19 July 2023 (Wednesday, 2.00pm SGT): UK inflation rate

Last month headline inflation in the UK held steady at 8.7% year-on-year (YoY), above market expectations for a fall to 8.4%. Alarmingly core inflation rose to 7.1% YoY, the highest since March 1992, and above market consensus for a rise of 6.8%.

This month (June), the market is looking for headline inflation to rise by 8.3% YoY from 8.7% in May. The UK rates market is pricing in 110p of rate hikes from the BoE over the next eight months, with a peak BoE terminal rate of 6.1% viewed in March next year.

After monthly GDP in the UK fell by -0.1% this week, it does underline the threat of stagflation for the UK economy, particularly if inflation fails to cooperate again this month.

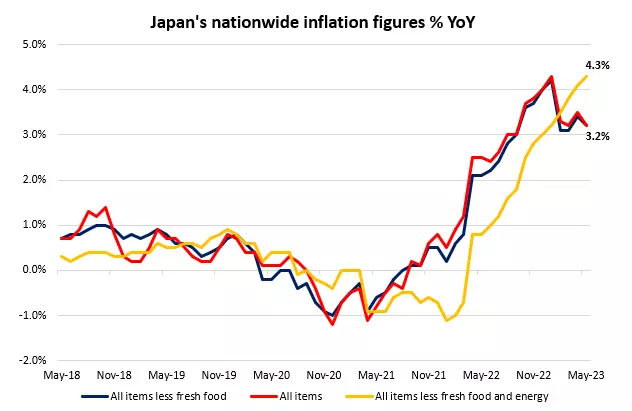

21 July 2023 (Friday, 7.30am SGT): Japan’s inflation rate

A recent pull-ahead in Japan’s wage pressures in May (2.5% versus 0.7% forecast) has challenged the Bank of Japan (BoJ)’s long-lasting view of inflation being ‘transitory’. In the aftermath of the data release, Japanese 10-year bond yields head higher, which reflects rising market bets for a quicker policy shift from the central bank, alongside a pick-up in the Japanese yen.

The next BoJ meeting lies just two weeks away and with chatters that the central bank may tweak its yield curve controls sooner rather than later, the upcoming inflation data will be on watch to validate such expectations. Over the past four months, there has been a divergence between the “core core” aspect of inflation (less food and energy prices) against the headline figure.

Another pull-ahead in “core core” inflation this week (currently 4.3%) will continue to widen the gap with the central bank’s 2% target, which may raise the odds of pricing pressures being more ingrained. That will likely support further hawkish positioning in the lead-up to the BoJ July meeting and aid to underpin the Japanese yen in the near term.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.