Key events to watch in the week ahead: 15 - 21 January 2024

What are some of the key events to watch next week?

This week’s overview

This week marked a week of recovery for Wall Street, after major US indices kickstarted 2024 on the backfoot with some profit-taking. Big tech stocks saw renewed traction, aiding growth sectors to pull ahead with stellar gains. Notably, Nvidia is up to a new record high with a 14% gain for the week, while Amazon and Meta Platforms are up 7%.

On the macro front, both the December headline and core US consumer price index (CPI) surprised slightly on the upside, but market participants were not buying into the stance that the Federal Reserve (Fed) will delay rate cuts because of a single data, while economic risks persist in the economy.

Expectations for a 25 basis point (bp) cut in March this year were firm, proving that there is little in its way for now. Ahead, attention will be turned to the US earnings season to validate views that corporate earnings have bottomed out and are set on a continued recovery path.

Heading into the new week, here are five things on our radar.

US earnings season: Morgan Stanley, Goldman Sachs, Interactive Brokers, Charles Schwab

The earnings season will continue with notable results from Morgan Stanley (24 Hours), Goldman Sachs, Interactive Brokers and Charles Schwab. It may seem like a relatively quiet week for earnings, before the busy schedule for big tech comes up in the Week of 22 January (Microsoft, Netflix, Tesla).

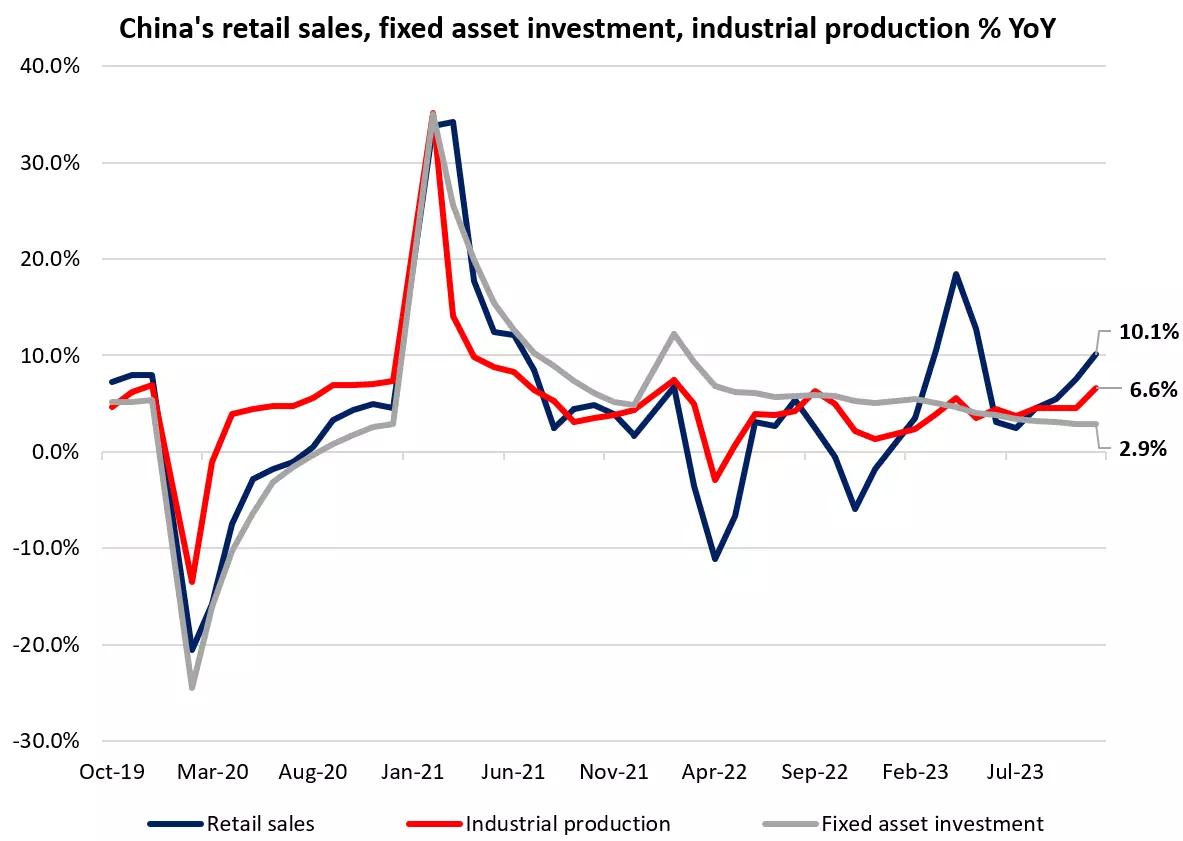

17 January 2023 (Wednesday, 10am SGT): China’s 4Q gross domestic product (GDP), fixed asset investment, industrial production, retail sales

This week, declining prices in December continue to reflect weak domestic demand in the world’s second largest economy, as soft labour conditions and a property market slump continue to keep consumer confidence at bay.

Despite a ramp-up in liquidity injections from the People's Bank of China (PBoC), alongside supportive measures for its property sector, the trend of weak economic data suggests that the accommodative policy environment has yet to translate to a sustained turnaround in economic conditions.

Ahead, broad expectations are for China’s growth headwinds to persist in 2024. Consensus is for December retail sales to firm to 11.0% from previous 10.1%, but it may be contributed by low-base effect from the previous year. Industrial production may ease to 6.3% from previous 6.6%, while fixed asset investment may stay muted at 3%. Any downside surprises in the data may reinforce the trend of weak growth conditions for China, amplifying calls for more to be done by authorities over coming months.

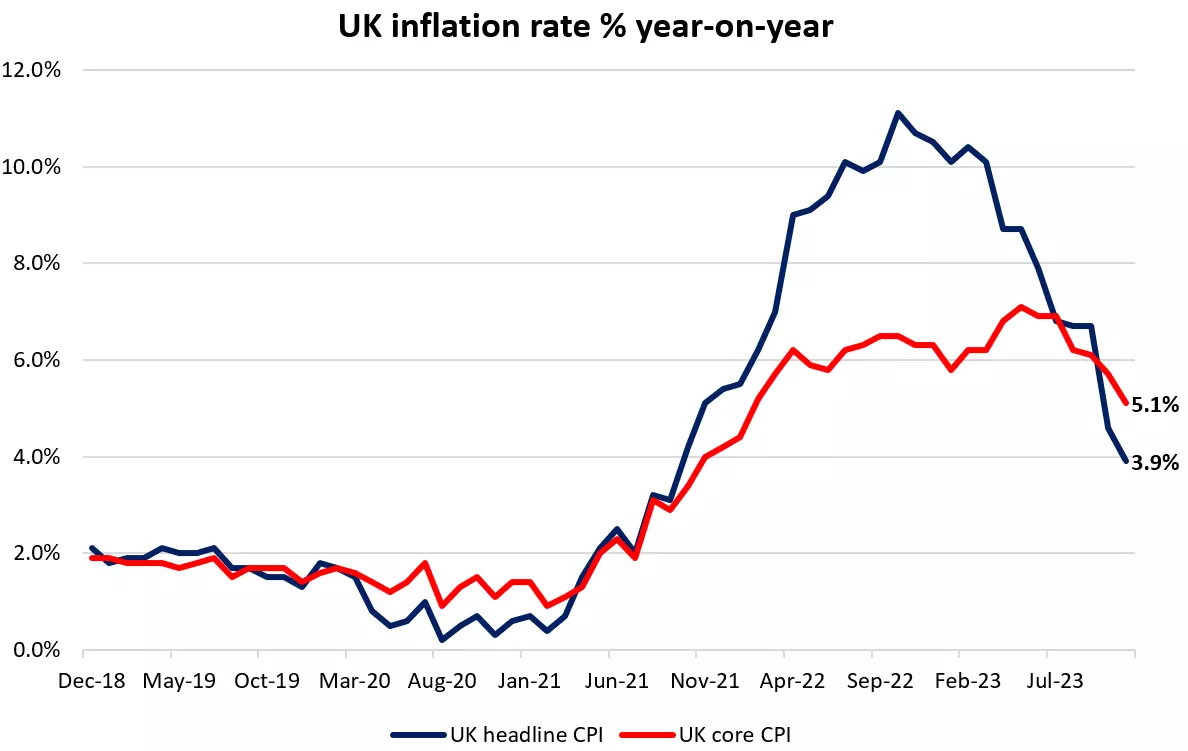

17 January 2023 (Wednesday, 3pm SGT): UK inflation rate

In the UK, annual inflation fell to 3.9% in November, its lowest rate in two years and below expectations of 4.4%. Core inflation fell for a fourth consecutive month to 5.1% in November from 5.7% in October.

The larger-than-expected falls in inflation is evidence that the Bank of England (BoE)'s aggressive rate hiking cycle is bringing inflation under control and has fostered expectations of six BoE 25 bp rate cuts in 2024.

Ahead, the market is looking for December headline inflation to remain at 3.9%, a monumental achievement given that inflation was hovering at 10.5% a year ago.

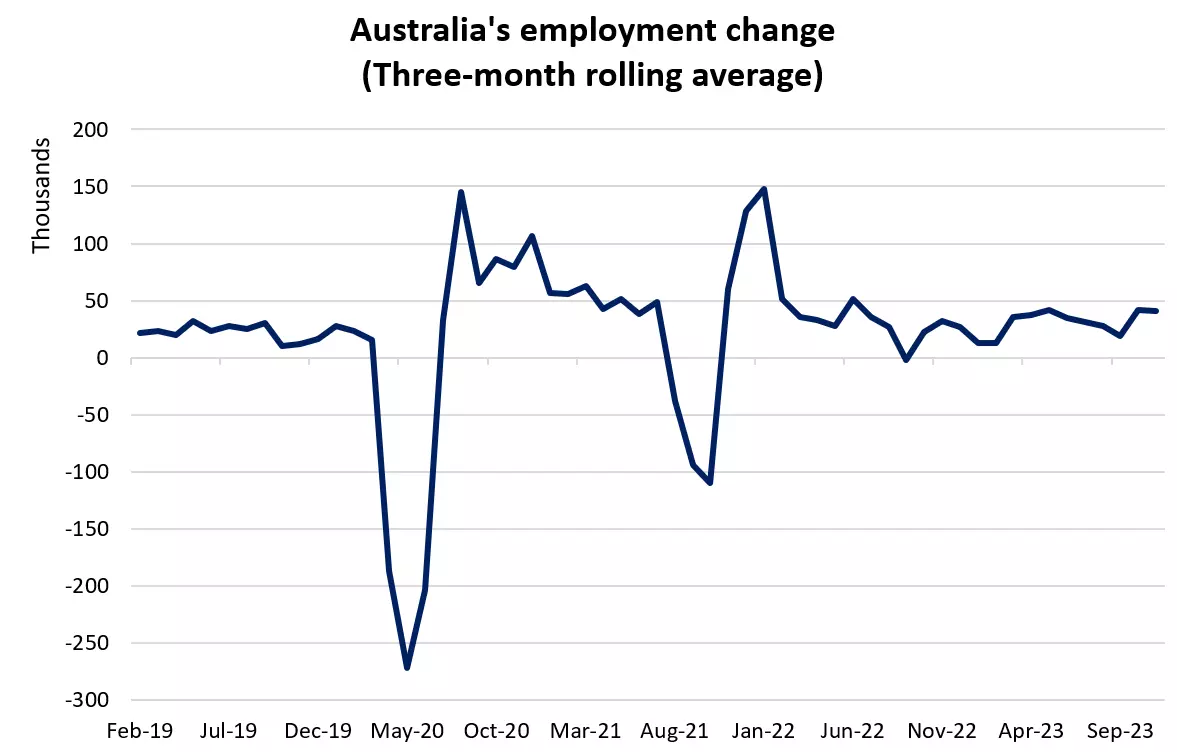

18 January 2023 (Thursday, 8.30am SGT): Australia’s employment change

The Australian economy added 61.5k jobs in November versus the 11.5k expected. The unemployment rate rose to 3.9% from 3.8%, as the participation rate surged to a record high of 67.2% from 67%.

This month (December), the market is looking for a +15k rise in employment and for the unemployment rate to remain unchanged at 3.9%. The participation rate is also expected to remain unchanged at 67.2%.

Into the upcoming jobs report, there are two Reserve Bank of Australia (RBA) rate cuts priced into the Australian rates market, with a first-rate cut priced for June and a second by December, which would take the cash rate back to 3.60% by year-end. If the unemployment rate ticks up to 4% or above, it may see the start of a third rate cut priced into the rates curve for 2024.

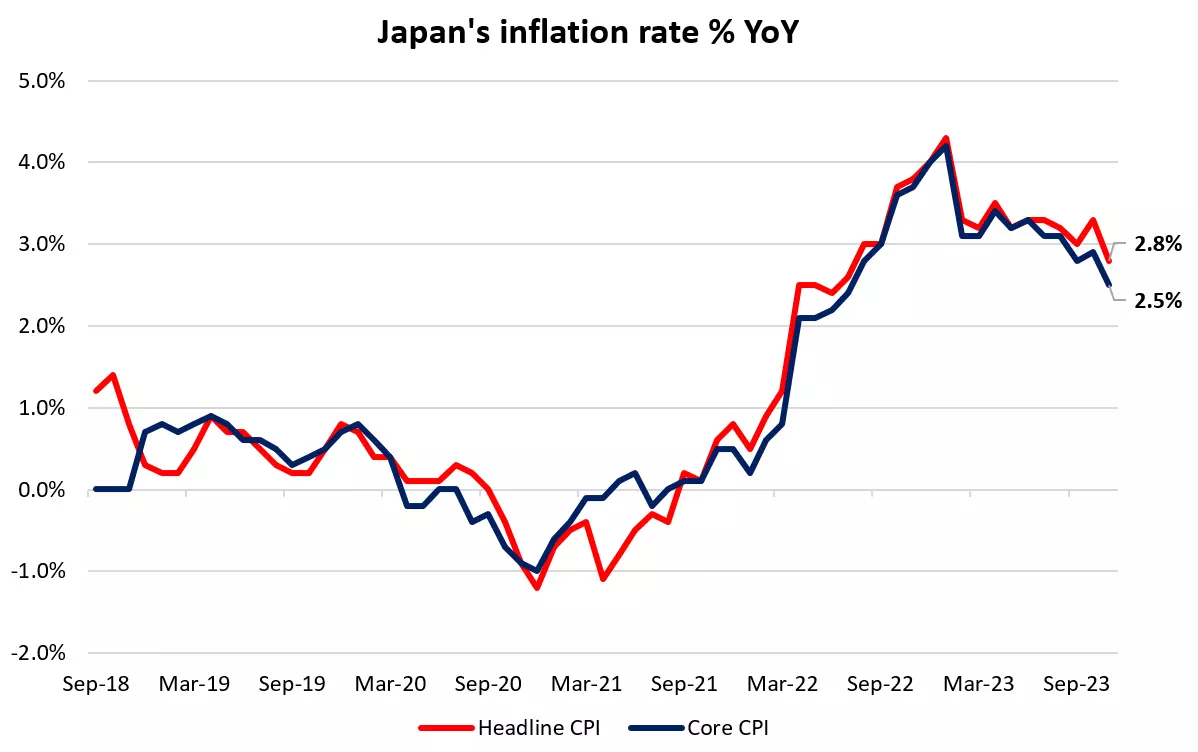

19 January 2023 (Friday, 7.30am SGT): Japan’s inflation rate

The Bank of Japan (BoJ) remains on the lookout for sustained wage increases and stable 2% inflation as conditions for a pivot away from its ultra-accommodative policies. But with the downside surprises in Japan’s November household spending and wage growth this week, recent data suggests that the BoJ still has room to exercise more patience in its policy normalisation process for now.

The upcoming inflation data will play an important role in swaying market expectations around the timing of exit for Japan’s negative-interest-rate policy. With Tokyo’s headline and core CPI data easing to their lowest levels since June 2022, it suggests that a similar disinflationary trend may play out for the nationwide inflation as well.

Expectations are for Japan’s December headline inflation rate to ease to 2.6% year-on-year from previous 2.8%, while the core aspect may ease to 2.3% from previous 2.5%. The data may still fall short of BoJ’s condition of a ‘stable’ 2% inflation, which may prompt more wait-and-see from the central bank at the upcoming January meeting.

IGA, may distribute information/research produced by its respective foreign affiliates within the IG Group of companies pursuant to an arrangement under Regulation 32C of the Financial Advisers Regulations. Where the research is distributed in Singapore to a person who is not an Accredited Investor, Expert Investor or an Institutional Investor, IGA accepts legal responsibility for the contents of the report to such persons only to the extent required by law. Singapore recipients should contact IGA at 6390 5118 for matters arising from, or in connection with the information distributed.

The information/research herein is prepared by IG Asia Pte Ltd (IGA) and its foreign affiliated companies (collectively known as the IG Group) and is intended for general circulation only. It does not take into account the specific investment objectives, financial situation, or particular needs of any particular person. You should take into account your specific investment objectives, financial situation, and particular needs before making a commitment to trade, including seeking advice from an independent financial adviser regarding the suitability of the investment, under a separate engagement, as you deem fit.

No representation or warranty is given as to the accuracy or completeness of this information. Consequently, any person acting on it does so entirely at their own risk. Please see important Research Disclaimer.

Please also note that the information does not contain a record of our trading prices, or an offer of, or solicitation for, a transaction in any financial instrument. Any views and opinions expressed may be changed without an update.

Seize a share opportunity today

Go long or short on thousands of international stocks.

- Increase your market exposure with leverage

- Get spreads from just 0.1% on major global shares

- Trade CFDs straight into order books with direct market access

Live prices on most popular markets

- Forex

- Shares

- Indices

See more forex live prices

See more shares live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 15 mins.

See more indices live prices

Prices above are subject to our website terms and agreements. Prices are indicative only. All shares prices are delayed by at least 20 mins.